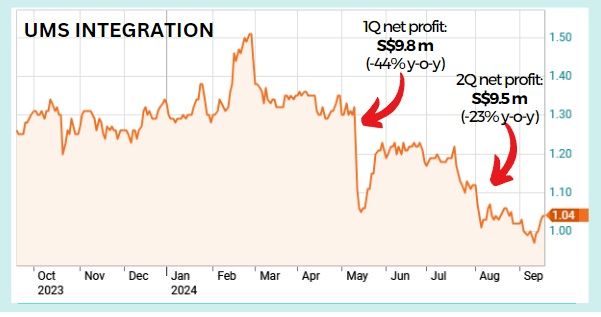

| 12 months ago, investor hopes were high for the share price of UMS Integration (fka UMS Holdings). UOB KH recommended a 'buy" on the stock ("Well-positioned for semicon recovery") while DBS Research named UMS as its "preferred pick" to ride the semiconductor industry recovery. The stock did edge up from $1.26 last Sept, reaching $1.51 in Feb 2024. Then it nose-dived following disappointing quarterly results (see chart):  Chart: Reuters Chart: ReutersThe problem stemmed from "weaker global chip demand," said UMS, which manufactures high precision front-end semiconductor components and performs complex electromechanical assembly and final testing services. Maybank Kim Eng reckoned UMS had lost market share with its key customer, Applied Materials, decreasing to 50-70%, from 75% previously. |

Against this backdrop, interestingly, UMS announced in July 2024 that it was seeking a secondary listing on Bursa Malaysia.

UMS has a significant manufacturing footprint in Malaysia, which has an established semiconductor eco-system.

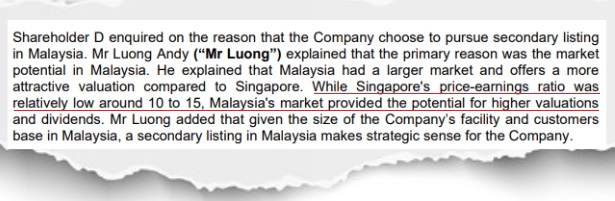

Reasons for giving Malaysian investors easier access to its shares were articulated by Andy Luong, UMS' executive chairman and CEO, at an EGM to approve a change of the company name.

Minutes of the EGM were released last week: Source: EGM minutes

Source: EGM minutes

So UMS is hoping for a higher valuation for its stock, somewhere at the same level as its peers in Bursa? What would that be?

Check it out:

|

Company |

Price (local currency) |

Market cap (local currency) |

Trailing PE |

P/BV |

Debt/Equity (%) |

Trailing dividend Yield % |

|

UMS |

1.03 |

710.5 |

13.6 |

1.7 |

2.77 |

5.6 |

|

Bursa Malaysia-listed peers |

||||||

|

Inari Amertron |

3.04

|

11.5B |

36.5 |

4.2 |

0.53 |

2.57 |

|

Malaysian Pacific Industries |

27.62 |

5.4B |

60.2 |

2.6 |

4.5 |

1.29 |

|

Unisem (M) |

3.20 |

5.1B |

69.6 |

2.2 |

7.95 |

2.55 |

|

ViTrox Corp |

3.28 |

6.1B |

58.9 |

6.1 |

5.86 |

0.19 |

|

Source: Yahoo! |

||||||

Andy Luong, chairman and CEO of UMS Holdings -- and JEP Holdings. NextInsight file photo.Indeed the Bursa companies are trading at much higher PE valuations than UMS, to the point of disbelief.

Andy Luong, chairman and CEO of UMS Holdings -- and JEP Holdings. NextInsight file photo.Indeed the Bursa companies are trading at much higher PE valuations than UMS, to the point of disbelief.

In searching for some clue on Malaysian Pacific Industries, for example, we found a recent article that says "estimates from the six analysts covering the company suggest earnings should grow by 22% each year over the next three years."

Similarly for Unisem, as another article said: "EPS is anticipated to climb by 42% per year during the coming three years according to the seven analysts following the company."

Despite its sky-high PE, ViTrox's prospects look relatively muted, with analysts forecasting a 16% rise in earnings for 2024. As for Inari, you can read a similar story here.

High PE = high growth expectations by the market.

Meanwhile, Singapore analysts are downbeat on UMS's near-term outlook. For example:

| • Maybank Kim Eng's Aug 2024 report expects a (30%) fall in net profit in 2024, followed by a 28% and 25% rise in the next 2 years. That's quite decent growth but the analyst's current target price is 85 cents with a "sell" recommendation. • CGS International's May 2024 report was more pessimistic, expecting a (25.4%) contraction in net profit in 2024, followed by only a 11.6% and 5.8% growth in the next two years. |

| So will UMS get a great reception on Bursa when it gets listed there sometime in 1H2025? Only time will tell. A caveat: As the company says, there's no assurance that it will even achieve the secondary listing. One last point, one to give some weight to: Andy Luong bought 600,000 UMS shares last week. His average price: 98.25 cents. His investment horizon, needless to say, is far longer than many investors'. |