| • There's very strong initial demand for Xiaomi's first EV model. Yes, Xiaomi whose brand we have long associated with mobile phones and home devices. • Launched at end-March 2024, its electric car is sold with better-than-anticipated gross margins -- but few investors would say that 5-10% are sexy figures.  Xiaomi is leveraging its strong brand recognition and large user base from its smartphones and AIoT products to cross-sell EVs. Xiaomi is leveraging its strong brand recognition and large user base from its smartphones and AIoT products to cross-sell EVs.• What's more, Hong Kong-listed Xiaomi still has to make significant investments in R&D and production capacity in order to reach profitability in its EV business over the next few years. • That's another reason for saying it's not exactly a great business. But it's one which will ride on mass adoption of EVs globally in the years ahead. • And it's an upbeat story of yet another Chinese brand making inroads globally and competing with legacy Western and Japanese brands. Read UOB KH's latest report on the company.... |

Excerpts from UOB KH report

Analyst: Johnny Yum

Xiaomi Corp (1810 HK)

| Stronger Confidence In EV Business After Investor Day And Factory Visit |

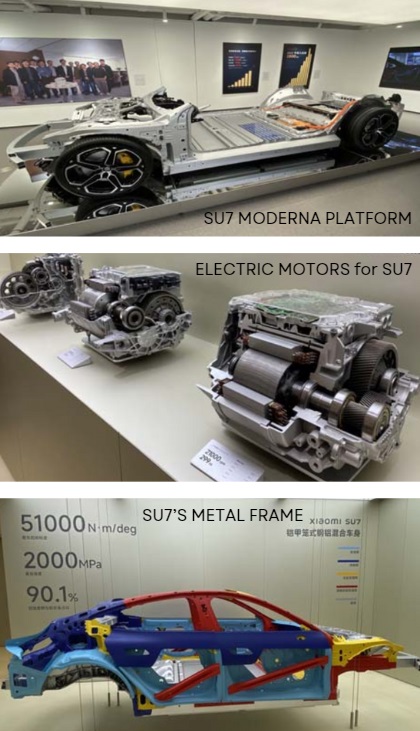

| We attended Xiaomi’s investor day and visited its EV production base in Beijing. During the event, the company disclosed encouraging developments for the EV business, including:

Maintain BUY and adjust target price to HK$21.00. |

| WHAT’S NEW |

• Some 75,723 units of locked orders, target of shipment of 100,000 units for full-year 2024 is another beat.

|

XIAOMI |

|

|

Share price: |

Target: |

As of 24 April, Xiaomi Corp’s (Xiaomi) SU7 locked orders (锁单, equivalent to other brand’s definition of “firmed orders” or 大定) reached 75,723 units.

This compares to around 70,000/40,000 units as of 20 April/2 April, which indicates that orders momentum remained strong since launch.

Xiaomi had started to deliver the standard SU7/SU7 Max models two weeks earlier than the original schedule, with total delivery reaching 5,781 units as of 24 April.

Xiaomi is now targeting to ship 10,000 units by June, and 100,000 units for full-year 2024. This is higher than our/market expectations of 50,000 and 80,000 units respectively.

| "We understand that Xiaomi had already started to prepare for the construction of the phase 2 plant, and the entire construction and ramp-up process may take around two years’ time. As such, Xiaomi’s EV business may reach breakeven in 2026-27 earliest." -- UOB KH |

• Positive gross margins of 5-10% are a big positive takeaway, given that market was expecting a gross loss of 5-15% for the electric vehicle (EV) business in 2024.

• High-end SU7 Max model dominates the sales mix at 43% of locked orders. The baseline SU7 and SU7 Pro model each contributed to 28-29% of total orders.

• R&D on EV business will continue to surge. Xiaomi is targeting to spend Rmb11b-12b in R&D on the EV business (vs around Rmb6.7b in 2023) and Rmb24b for the entire group in 2024. This is higher than our estimates of Rmb7b and Rmb20b respectively.

• Breakeven at annual shipment of 300,000-400,000 units. Given that the phase 1 EV factory has a designed maximum annual capacity of only 150,000 units, Xiaomi will have to construct its phase 2 factory in order to reach the breakeven target.

We understand that Xiaomi had already started to prepare for the construction of the phase 2 plant, and the entire construction and ramp-up process may take around two years’ time. As such, Xiaomi’s EV business may reach breakeven in 2026-27 earliest.

• Market feedback on user experience. We believe the SU7 series is well positioned as a performance EV sedan – great feedback in terms of driving experience, better seat designs and larger head/leg rooms.

However, the passenger’s experience, more notably for the backseat, received more criticism given the narrower space.

As such, while Xiaomi’s SU7 is well received as a performance model, we believe it is likely less competitive as a family car compared with its peers such as Aito’s Luxeed brand.

| STOCK IMPACT |

• We revise up our EV sales assumptions to 90,000/150,000/190,000 units in 2024-26 respectively to factor in the much stronger-than-expected locked orders from consumers. This compares with our previous estimates of 50,000/120,000/160,000 units.  • We also revise up EV business’ margin assumptions to 5.0%/8.5% in 2024-25 respectively, compared with our previous estimates of -15%/-5%.

• We also revise up EV business’ margin assumptions to 5.0%/8.5% in 2024-25 respectively, compared with our previous estimates of -15%/-5%.

Our margins assumptions are on the conservative side, as we expect a sustained margin pressure across the entire EV market due to intensifying competition. Our assumption for 2026 onwards remains unchanged at 10% for now.

• We also raise our opex assumptions for the EV business from Rmb7b-9b in 2024-26 to Rmb11b-12b in order to factor in the higher-than-expected R&D spending guidance.

• Changes for non-EV business. We factor in a stronger-than-expected 1Q24 shipment (40.8m units, vs our estimates of 35m units), and Xiaomi’s better-than-expected share gains in both China (+0.2ppt to 14.6% in 1Q24 despite competition from Huawei), and overseas (+1.2ppt yoy to 14.8% in 1Q24), and raise our smartphone shipment assumption to 163m/170m/180m units in 2024-26 respectively.

We also raised our opex ratio assumption for the non-EV business as we expect increased activities in the overseas market to incur a higher cost.

| EARNING REVISION/RISK |

• We factor in a higher operating expense, primarily due to EVs’ high R&D expenses, and our net profit estimates are trimmed by 15.7%/4.0%/9.0% to Rmb13.5b/16.9b/21.1b respectively.

|

Stock price |

HK$17.36 |

|

52-week range |

HK$9.86 – 17.34 |

|

Market cap |

HK$433 B |

|

PE (trailing) |

22.6 |

|

Dividend yield (trailing) |

-- |

|

1-year return |

57% |

|

Net profit margin |

6.45% |

|

Source: aastocks |

|

Our non-EV (core) business net profit estimates ended up largely unchanged, as the higher smartphone sales was mostly offset by a higher non-EV opex.

• Main risk now lies in production ramp-up. If Xiaomi falls behind in production schedule, the long order lead time may incentivise customers to switch to other brands.

This is especially the case, as market news indicate that some competitors are now offering to provide subsidy for the non-refundable down-payment (Rmb5,000 for Xiaomi) if the buyers are to switch to their brand.

As such, if Xiaomi somehow fails to deliver its production rampup, we see potential downside risks to our shipment estimates.

• Maintain BUY and adjust target price to HK$21.00, based on:

The valuation for the EV business also implies 0.7x 2024F P/S, which is very conservative, as the market is now valuing the EV business at 1x P/S. Our more conservative view stems from the still-limited track record, as well as concerns of an intensifying competition in China’s EV market. |

Full report here.