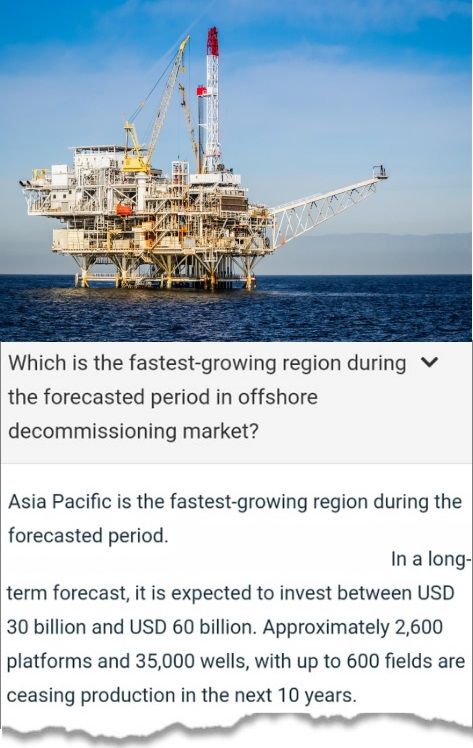

| As oil fields at sea eventually run out of reserves that are economical to extract, their infrastructure has to be decommissioned by law. Decommissioning work is complex and dangerous. It involves, among other things, the removal and disposal of platforms and pipelines, etc ensuring that the site is left in an environmentally acceptable condition. Offshore decommissioning is at an infancy stage across the world with Asia-Pacific forecasted to be the fastest-growing region:  Source. Source. Southeast Asia, where many fields such as those in the Gulf of Thailand, have been in production for several decades, will see its share of decommissioning projects. Call it a sunrise industry. And there's one Singapore listco that is, of late, achieving a surging orderbook for decommissioning projects -- Mermaid Maritime, which is headquartered in Thailand. And over the past 12 months, Mermaid's stock has risen from ~7 cents to ~12 cents. |

Back in July 2020, recognising the decommissioning opportunity, Mermaid established a Transportation, Installation (T&I) and Decommissioning services business unit.

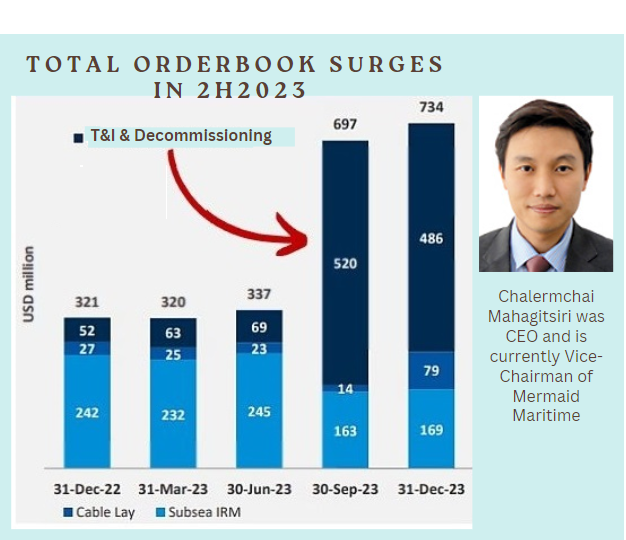

At that time, Mermaid's CEO, Mr. Chalermchai Mahagitsiri, said:

Chalermchai Mahagitsiri was CEO and is currently Vice-Chairman of Mermaid Maritime“The potential for future decommissioning work is expected to increase in 2021 and continue over the next 10-20 years. In particular, the Gulf of Thailand has over 400 offshore platforms with an estimated 100 platforms to be approved by the Thai government for decommissioning over the next 10 years. Chalermchai Mahagitsiri was CEO and is currently Vice-Chairman of Mermaid Maritime“The potential for future decommissioning work is expected to increase in 2021 and continue over the next 10-20 years. In particular, the Gulf of Thailand has over 400 offshore platforms with an estimated 100 platforms to be approved by the Thai government for decommissioning over the next 10 years. "With this initiative by Mermaid, we have become the first Thai-owned and Thai-operated services company in the Offshore Transportation, Installation and Decommissioning sector having the capability to deliver services of an international standard using qualified local content for the Thailand market." |

Mermaid's T&I and Decommissioning orderbook surged in the 2H of last year, as the chart below shows:  Chart: Company

Chart: Company

The orderbook for T&I and Decommissioning comprises work for both new and old topsides.

Transport & Installation, as the name suggests, pertains to work for new topsides and pipelines. (Topside refers to parts of a drilling platform that are above the waterline. Topsides often include the drilling rig, living accommodation, and processing facilities)

Decommissioning is obviously to do with old topsides and old pipelines.

(Given that the orderbook for the segment became significant in 2H2023, which was 4 years after the business unit was set up, perhaps the reporting for T&I and for decommissioning should be segregated by Mermaid for greater transparency from now).

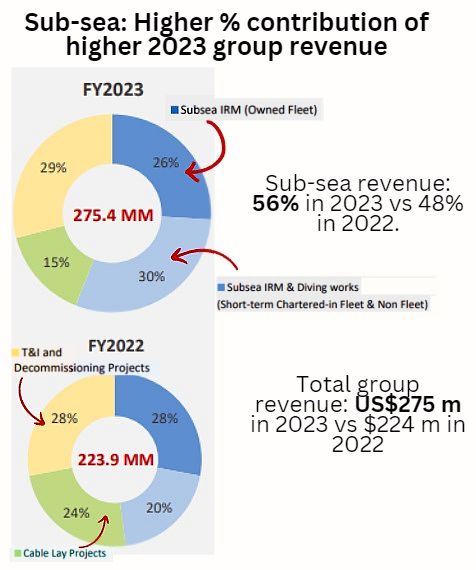

| While its decommissioning business is rising, Mermaid continues to see robustness in one of its core business -- subsea IRM (inspection, repair and maintenance) -- which is supported by strong oil prices. IRM's contribution to group revenue in 2023 rose 43% y-o-y to US$154.2 million (see chart below) although the end-2023 orderbook for IRM was lower than in 1H2023.  Mermaid carries out annual inspection, repair, and maintenance programs for Saudi Aramco and national oil companies. "These key clients have shown resilience against capital expenditure reductions," said Mermaid in its annual report 2023. |

While profits are set to continue to roll in, Mermaid doesn't look ready to pay a dividend to shareholders anytime soon.

|

Year |

Net profit US$’m |

|

FY17 |

4.2 |

|

FY18 |

- 27.3 |

|

FY19 |

-24.2 |

|

FY20 |

-109.6 |

|

FY21 |

-15.7 |

|

FY22 |

-0.3 |

|

FY23 |

9.7 |

Until it reported US$9.7 million net profit for 2023, it had suffered 5 straight years of losses totalling US$177 million (see table).

Reasons for the losses: A downturn in the oil & gas sector slashed demand for Mermaid's services; vessel market oversupply; disruptions caused by Covid-19 pandemic; asset impairments and restructuring costs, etc.

Given the multi-year of losses, Mermaid ran low on operating cashflow and survived on loans from its parent company, Thoresen Thai Agencies.

As at end-2023, it had US$81.3 million outstanding debt:

| • USD 14.6 million of short‐term loans (consisting of USD 3.1 million from financial institution and USD 11.5 million from parent company) and • USD 66.7 million of long‐ term loans (consisting of USD 24.2 million from financial institution and USD 42.5 million from parent company). |

A not small amount -- US$38 million -- is due for repayment in 2024, and Mermaid said its short‐term liquidity risk is "low".

As at end-2023, Mermaid had US$30 million cash and cash equivalents plus another US$15 million as a restricted deposit with financial institutions.

Subsequently, in Feb 2024, Mermaid announced US$55 million of additional loans from its parent company.

This is for working capital for subsea pipe laying operations and the transportation, installation and decommissioning projects that were awarded by a leading petroleum exploration and production company in Thailand, said Mermaid.

Is Mermaid's parent also banking on a turnaround story, a vigorous turnaround story driven by a sunrise sector called decommissioning?