| Thakral Corp has a big challenge and it's not profit. It has just embarked on an investor relations journey to make investors sit up and appreciate its new businesses and their potential. Its stock trading liquidity has been low and continues to be low. Compared to its price 1-year and 2-years ago, the stock has barely budged. Investors need greater familiarity and clarity about its current businesses and maybe shed impressions about its previous electronics distribution business which has long been divested.  At GemLife resorts, a pool is among the amenties provided to its homeowners who are typically retirees who pay 100% cash upfront for their homes. At GemLife resorts, a pool is among the amenties provided to its homeowners who are typically retirees who pay 100% cash upfront for their homes. Emerging in recent years, Thakral's "star performer", as its CEO describes it, is a property business in Australia. And it's now by far the largest component of its core operations in terms of net assets as well as profitability. It's not the usual property business model that Singapore investors are familiar with. |

GemLife was co-founded in 2016 by Thakral and the Puljich family who are seasoned real estate investors. Thakral has a 31.7% stake in GemLife, which acquires land sites, develops and operates resorts for people who are typically over 50 years of age, mainly retirees.

Thakral has a 31.7% stake in GemLife, which acquires land sites, develops and operates resorts for people who are typically over 50 years of age, mainly retirees.

It's a niche model in Australia.

GemLife fully sells the house but retains the land, so homeowners pay a weekly lease fee of about A$200.

In other words, there's profit from the sale of house and recurring revenue from the land lease.

Where do we find the contribution of this business in Thakral's P&L statement?

It's in the "share of profit of associates and JV" and the sub-category "investment segment".

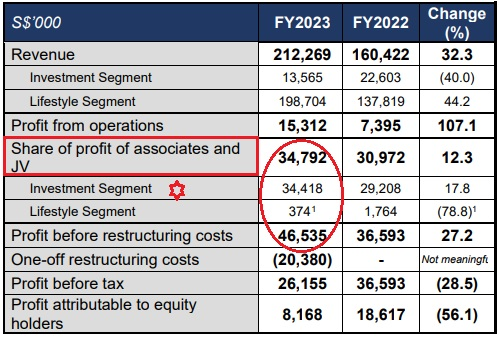

• The "investment segment"profit of S$34.4 million includes a relatively small contribution from 6 co-invested office properties in Japan. • It also includes a S$3.1 million profit from the divestment of a JV of a beauty business in China. In all the S$34.4 million made up 74% of Thakral's profit before restructuring costs. • Thakral did an internal restructuring exercise (more below) for its Australian business, resulting in a one-off charge of S$20.4 million arising principally from settlement of costs payable to minority shareholders. • Excluding this restructuring cost, Thakral recorded a segmental profit growth of 19.6% yoy to S$44.6 million. |

What was that internal restructuring exercise that Thakral was willing to pay S$20.4 million for?

• Thakral had a subsidiary, Thakral Capital Holdings (TCH). • Thakral had a subsidiary, Thakral Capital Holdings (TCH). • A group of Australian executives, who were also employees tasked to grow a range of TCH's real estate business in Australia, held a 25% stake in TCH. • Thakral decided to focus on GemLife as it was fast-growing and held the best potential, and it was agreed that the executives would sell their interest in TCH to Thakral, so TCH became a wholly-owned subsidiary of Thakral. • They also agreed to cancel their options under the TCH employee share option scheme for a fee and received contractual bonus entitlements. |

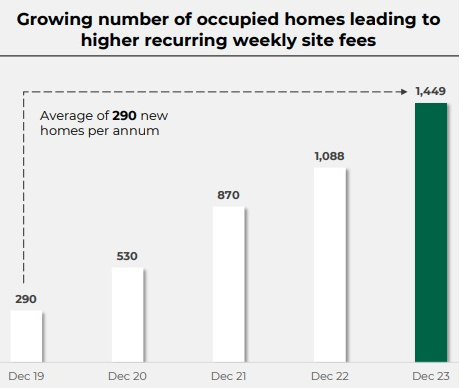

GemLife is targetting to sell 6,500 occupied homes within a decade and is actively exploring opportunities to ramp up development.

The target, if achieved, represents an accelerated growth rate, averaging 500 homes a year over the next 10 years (after accounting for the 1,449 already built).

Meanwhile, there's Thakral's "lifestyle segment", though a still small contributor to profits, which bears watching because it may grow faster than previously. This segment comprises:

| • Thakral has a 10% stake in UK-based private company, CurrentBody, which is an online retailer of a variety of devices for at-home use, including those for anti-aging, acne treatment, facial cleansing, and hair removal. CurrentBody has turned profitable. • In China, Hong Kong and Macau, the Group focuses on the management and marketing of leading premium beauty, fragrance and lifestyle brands • In South Asia, Thakral is the exclusive distributor of DJI, the world's largest drone manufacturer.  |

|

Thakral had S$8.7 million cash as at end-2023, down from S$16.8 million a year ago due to the restructuring costs, new investments and dividends (S$2.6 million) paid to shareholders.

|

For more info, see Thakral's FY2023 PowerPoint deck here.