|

Two weeks ago, I mentioned that some Reits’ charts (click HERE) have caught my attention. On a fundamental basis, besides Lendlease Reit (Click HERE for key takeaways from my 1-1 meeting with Lendlease Reit Manager CEO), Sasseur Reit has caught my attention. |

Below are my key takeaways and what I gather from analyst reports and other readings.

Description

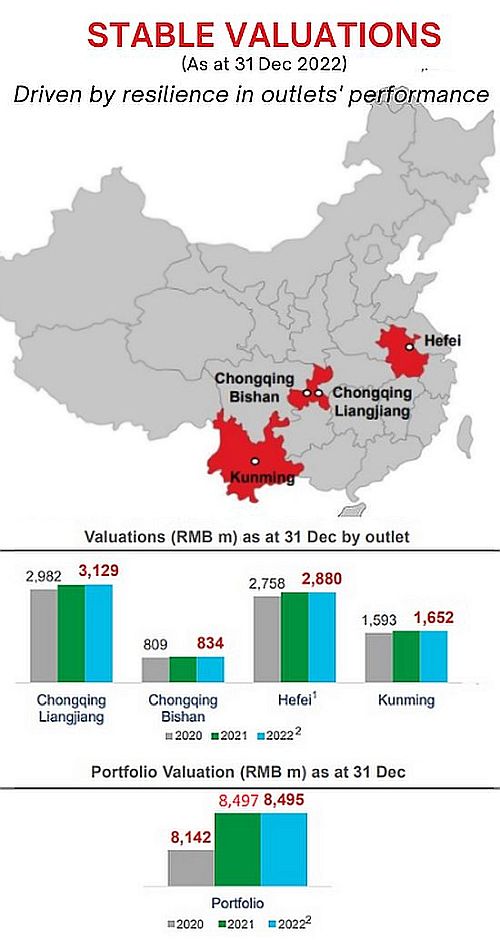

Sasseur Reit is the first retail outlet mall Reit listed in Asia. It has four retail outlet mall assets located in Chinese cities namely Chongqing, Kunming and Hefei, with a combined net lettable area of 310,241 square metres. 1. Hefei's valuation is only reflective of Sasseur REIT’s ownership stake in the outlet, which is approximately 81% of total gross floor area.

1. Hefei's valuation is only reflective of Sasseur REIT’s ownership stake in the outlet, which is approximately 81% of total gross floor area.

2. Based on independent valuation as at 31 Dec 2022 by Colliers Appraisal & Advisory Services Co., Ltd.

Why am I interested in Sasseur Reit?

| A) Interesting business model |

Sasseur Reit is the first retail outlet mall Reit listed in Asia.

The outlet concept first started in China in 2002 as “factory outlets” which specialised in clearing excess inventories. Over time, it morphed into a large scale shopping mall concept which emphasises on a combination of brand and value.

Sasseur Reit outlets typically sell off-season products at a discount of at least 20-30% and in-season products are sold at a discount of at least 10%.

Tenants at Sasseur Reit are only allowed to sell authentic products. If they are found not authentic, the tenant has to pay 10 times the value of the sale product.

Furthermore, the average growth rate of outlets in China has been accelerating. The estimated sales revenue of China’s outlets is targeted to reach RMB950b in 2027.

| B) Analysts are positive |

Source: Bloomberg

Source: Bloomberg

Six analysts cover Sasseur Reit with either buy or add calls and target prices $0.90 – 1.10.

Based on the closing price of $0.720 on 21 Jul, coupled with the estimated dividend yield of around 8.9%, total potential return is approximately 39.5%.

It is noteworthy that KGI is not captured in the Bloomberg screenshot above.

| C) China is supportive of domestic consumption |

Based on my readings, China continues to boost their domestic consumption which can be a powerful tool to spur economic growth, especially as exports are experiencing uncertainties from a potential slowdown in various countries and domestic investment is gradually reaching saturation.

Based on a report by the Development Research Center of the State Council cited in an article in China daily dated 8 May 2023 (click HERE), China’s middle income group will balloon 75% to 700m people, up from the current 400m. This should bode well for Sasseur Reit as this is precisely the target customer market segment which they are in.

Based on Sasseur Reit’s FY22 annual report, during the annual session of China’s National People’s Congress in March 2023, the government stressed on giving priority to the recovery and expansion of domestic consumption and boosting the incomes of urban and rural residents through multiple channels.

This bodes well for the country’s consumption outlook. The government had also announced plans to boost the scale of consumption and investment to a new level by 2035, significantly reduce income gaps between urban and rural residents, and make substantial progress in the country’s “common prosperity” drive.

| D) Main beneficiary among S Reits of China’s domestic consumption story |

Sasseur Reit has a unique entrusted management agreement model (“EMA”) which provides stability of EMA rental income via the fixed component and upside to be derived from higher sales via the variable component of the EMA rental income. For numerical examples of the EMA model, please click HERE on EMA numerical examples for the three scenarios where there is an excel spreadsheet to illustrate how its EMA model works.

| SIGNIFICANT VARIABLE |

| "Importantly, unlike most retail Reits in Singapore which charge mostly fixed rent and the balance being variable rent, Sasseur Reit has a significant contribution from its variable rent component. This places it as the main beneficiary among S Reits of China’s consumption story over the medium to long term." |

Importantly, unlike most retail Reits in Singapore which charge mostly fixed rent and the balance being variable rent, Sasseur Reit has a significant contribution from its variable rent component. This places it as the main beneficiary among S Reits to benefit from China’s consumption story over the medium to long term.

Notwithstanding the variable component, based on Phillip Securities’ report, in the worst-case scenario, if we assume that Sasseur Reit gets zero rent from its variable component, Sasseur Reit still provides at least 5.4% dividend yield from its fixed component rent alone.

It is also noteworthy that at the time of Phillip Securities report, Sasseur Reit was trading at $0.750. Sasseur Reit is now trading at $0.720, thus it should provide higher than 5.4% dividend yield from its fixed component rent now. This “worst case” yield is already higher than some of S Reits already.

| E) 2HFY23F may be stronger due to a myriad of factors |

As of 31 Mar 2023, Hefei and Kunming outlets have seen a decline in occupancy rate to 95.9% and 96.3% respectively. For Hefei, the decline was because Sasseur Reit has replaced some non performing F&B tenants with new F&B tenants who are scheduled to commence leases in 2Q 2023. Consequently, the occupancy rate is likely to improve either in 2Q or 3Q.

Kunming is a tourism spot where domestic travellers like to travel. Suffice to say that Sasseur Reit is optimistic that the occupancy rate should reverse its decline as domestic travel resumes. Based on a Straits Times article dated 30 Apr 2023, China’s tourism and consumer activities have sharply picked up. It cited 19.7 million railway trips were made across the country on 29 Apr, the highest on record for a single day. This may bode well for Sasseur Reit.

Furthermore, 2Q is typically the weakest. 4Q and 1Q are the strongest quarters especially 4Q due to Christmas. 3Q is likely to see a bump in sales as Sasseur Reit runs their annual Anniversary Sales event in 3Q.

With the above factors, it is likely that 2HFY23F is likely to be even stronger than 1HFY23.

| F) No significant refinancing till FY26 |

Based on The Edge 14 Jul 2023 writeup (click HERE) where it mentioned why refinancing of Chinese S-Reits and trusts takes longer, it is worth mentioning Sasseur Reit’s loans.

As of 30 Sep 2022, Sasseur Reit has loans amounting to approximately SGD500m which matures in Mar 2023. On 31 January 2023 Sasseur Reit entered into a 3-year secured facility agreement (with an option to extend for another two years at the discretion of the lenders) consisting of a term loan facility of S$125m and US$54m, and a S$10m revolving credit facility, with a group of lenders.

On 3 February 2023, Sasseur Reit entered into a 5-year secured facility agreement for an onshore term loan of RMB975m with a group of China based lenders. Also on the same day, Sasseur Reit obtained an unsecured interest-bearing loan of RMB308m (approximately SGD60m equivalent) from its sponsor with the option to be extended for up to another year, subject to mutual agreement.

Post refinancing, Sasseur Reit’s outstanding loans of a single maturity date are separated into several loans with differing maturities and with different lenders. This is a major strategic step and an incredible feat to reduce debt concentration risks.

Except for the sponsor’s $60m loan which expires in 2024, with an option to extend for another one year, Sasseur Reit’s subsequent refinancing requirements are in 2026. It is noteworthy that as of 31 Mar 2023, Sasseur Reit’s gearing is around 25.7% which is one of the lowest gearing among S Reits, if not the lowest. Sasseur Reit has ample debt headroom of around $861m for M&A based on MAS’ prescribed leverage limit of 50.0%.

| G) M&A – major catalyst if done properly |

Sasseur Reit has right of first refusal for two properties, namely Xi-an and Guiyang outlet malls. Personally, I think there are good odds that Sasseur Reit may exercise its right of first refusal on either Xi-An or Guiyang with Xi-An being the more likely target in the next one year. I arrive at this basis because

- According to management, Sasseur Reit’s sponsor is on an asset light model and they are very willing to sell.

- Sasseur Reit has not done any acquisition since its IPO on 28 Mar 2018.

- Sasseur Reit has recently refinanced almost S$500b debt due in Mar 2023 into several loans with differing maturities and with different lenders. This is an extremely significant and strategic step. Sasseur Reit has no major refinancing risks till 2026. In addition, they have managed to unencumber Kunming outlet. This is a strategic move as it increases the flexibility for Sasseur Reit to optimise its debt capacity for any potential acquisition.

- Sasseur Reit has mentioned a couple of times in their recent announcements about their plans for acquisitions. On 3 Feb 2023, Sasseur Reit in their press release (click HERE) also cited “the unencumbering is important…. in the pursuit of an asset acquisition in the near future”. Moreover, in Sasseur Reit’s ARFY22 report out in Apr 2023, they also wrote that apart from organic growth coming from active asset management, they are exploring appropriate accretive acquisition opportunities by leveraging the broad network and pipeline assets of the Sponsor.

- According to management, the portfolio valuation for Xi-an outlet mall has not increased much in FY22. In fact, it has remained stable in FY22. It may arguably be better to acquire earlier rather than later, before the portfolio valuation moves higher, a view shared by management.

Notwithstanding the above, I wish to emphasise that any M&A is likely to be a major price catalyst only if it is done properly. According to management, their first priority is to fund its acquisition with debt, instead of a combination of equity and debt.

It is noteworthy that Sasseur Reit has ample debt headroom $861m as of 31 Mar 2023. In addition, they prefer Xi-an outlet mall as it is as big as Chongqing Liangjiang in terms of sales but it’s a much younger asset. It is noteworthy that Chongqing Liangjiang contributes RMB268m in FY22 EMA Rental Income, equivalent to around 45% of entire FY22 EMA Rental Income. Therefore, a potential acquisition of Xi-An is extremely significant to Sasseur Reit.

| H) Attractive dividends |

Even during the depths of Covid, Sasseur Reit continued to pay out distributions on a quarterly basis as one of Sasseur Reit Manager’s key objectives is to provide unitholders with an attractive rate of return on their investment through regular and stable distributions.

If we assume that Sasseur Reit’s FY23F distribution is on par with that of FY22 distribution of SG 6.55 cts / share, this translates to an estimated dividend yield of around 9.1%.

Notwithstanding the weak RMB against SGD, I believe there is scope for FY23F distribution to be at least equivalent to that of FY22. In 1QFY23, distribution per share was SG1.849 cts per share, up 1.5% on a year-on-year basis.

| I) Portfolio valuation likely remains stable on a CNY basis but probably dips on FX |

Readers would have read (in horror) that Dasin Retail Trust’s valuation has tumbled 16% from RMB11.3b as at 31 Dec 2021 to RMB9.5b as at December 31, 2022.

Sasseur’s management does not see any sharp decline in valuation on a RMB basis as the outlets are still performing strongly in sales amid relatively high occupancy rates and resilient rents.

On a SGD adjusted basis, SGD has strengthened 4.3% against RMB from around SGDRMB: 5.1374 on 31 Dec 2022 to SGDRMB:5.3596 on 30 Jun 2023 which is likely to cause a decline in the valuation of its properties in SGD terms. Sasseur Reit assesses the fair value of investment properties on a yearly basis.

| J) Low valuations; 1.0x standard deviation below its average 2Y P/BV |

Based on Bloomberg, Sasseur Reit trades at an undemanding 0.8x FY22 P/BV, 1.0x standard deviation below its average 2Y P/BV of 0.9x. Based on analysts’ estimates, at $0.720, Sasseur Reit trades at 0.83x FY23F P/BV with a FY23F dividend yield of around 8.9%. NAV / share is around $0.863.

| K) Next dividend likely to be ex around 1st 2 weeks of Sep |

Sasseur Reit expects to report 1HFY23F results on 11 Aug 2023 before market opens. It gives dividends on a quarterly basis. Last year, Sasseur Reit’s 1HFY22 results was on 12 Aug and it ex div SG0.01588 on 9 Sep. If we assume that Sasseur Reit distributes the same amount of dividends (i.e., SG0.01588) in 2QFY23F, this works out to be 2.2% dividend gain in the near term.

| HIGHER PAYOUT |

| "DBS Research in its writeup pointed out that with the completion of refinancing and no significant asset enhancement initiative project in 2023, there is scope for a higher dividend payout ratio to around 95%." |

Although Sasseur Reit does not have a fixed payout ratio from quarter to quarter (given the seasonality factors of the outlet mall business), they are committed to pay out at least 90% of distributable income for the full year.

It is noteworthy that the dividend payout ratio for FY2021 and FY2022 was around 91% – 92%. DBS Research in its writeup pointed out that with the completion of refinancing and no significant asset enhancement initiative project in 2023, there is scope for a higher dividend payout ratio to around 95%.

It is noteworthy that Sasseur Reit’s 1QFY23 dividend payout ratio was around 96.3%, up from 91.5% in FY22. Amid this backdrop and perhaps offset to a certain extent by a weakening RMB, I guess odds are still good that Sasseur Reit should be able to distribute at least SG0.01588 as dividends in 2QFY23F.

| L) Sponsor – who is Sasseur Cayman Holding Limited? |

Sasseur Cayman Holding Limited is the Sponsor of Sasseur Reit. The Sponsor Group ranks among the top outlet player by number of outlets. It has about 30 years of experience in outlet mall operations. Since its opening of its first Sasseur outlet, Chongqing Liangjiang in 2008, it has grown from strength to strength to its 16th outlet in Fuzhou in 2022.

It intends to open two more outlets in Shijiazhuang (Oct 2023) and Urumqi (Sep 2024). The Sponsor has been supportive of Sasseur Reit and has signed an unsecured interest-bearing loan of RMB308m on 3 Feb 2023 with Sasseur Reit with the option to be extended for up to another year, subject to mutual consent.

Potential risks

As with almost all investments (if not all), they do carry risks. I am only listing some pertinent ones and this is not a comprehensive list. Please refer to the analyst reports HERE for more information.

| A) Business risks – weaker than expected leasing, slowdown or changes in consumer spending |

Weaker than expected leasing or / and a drop in tenant sales perhaps due to

- weaker than expected economic environment or;

- a surge in competition from other outlet malls or;

- if consumers choose alternative shopping options or;

- a sudden change in consumer preferences etc.

If any of the above happens, it is likely to have an adverse impact on Sasseur Reit. Sasseur Reit’s variable rent component is typically 4-5.5% of outlet’s sales, hence any weakness in tenant sales is likely to have an adverse impact on Sasseur Reit.

Notwithstanding the weaker than expected China economic data, management shares that even if consumers spend less on a per customer basis, the overall number of consumers spending at their malls is likely to increase over time.

| B) Short weighted average lease of expiry |

Sasseur Reit has a short weighted average lease of expiry – 2.1 years and 0.9 years by net lettable area (“NLA”) and gross revenue (“GR”) respectively. Sasseur Reit deliberately keeps their lease tenure short so that they have the flexibility to replace non-performing tenants with new successful brands so as to capture the ever-changing consumer preferences in China.

As at 31 Mar 2023, 47.7% and 64.9% of the leases by NLA and GR will expire in 2023 respectively. If Sasseur Reit fails to renew the leases with either existing tenants, or fail to find new quality tenants to replace non-performing ones, it may have an adverse impact on Sasseur Reit.

Notwithstanding this, management shares with me that Vito Xu, founder and chairman of Sasseur Group has a wealth of experience and connections in the fashion industry with numerous brands. It is typically not difficult to replace the tenants from their existing pool of connections.

| C) Possibility of equity fund-raising |

It is common knowledge that Sasseur Reit intends to do some M&A.

Although it is likely to fund the acquisition with debt, we will not know for sure whether it may fund it solely via debt, or a combination of debt and equity (only after it happens). A dilutive acquisition via equity may be viewed negatively by the market and may have an adverse impact on its share price.

| D) Sharper than expected interest rate hike |

As at 31 Mar 2023, Sasseur Reit’s debt currency profile comprises of 30% in SGD loan; 16% in USD loan and the balance in RMB loan. The rate for RMB loan is rather stable as it is pegged to China’s five-year loan prime rate. A portion of the USD and SGD loan is hedged.

In aggregate, 77.2% of the loans is either hedged or pegged to stable loan rates.

Nevertheless, it is noteworthy that every +/-50bps increase in interest rate translates to a -/+ SG 0.04 cents in distribution per unit (“DPU”) per annum. Thus, any sharper than expected interest rates hike may affect the interest expense which Sasseur Reit has to pay on their loans, resulting in a reduced DPU.

| E) China risk premium |

Negative news flow on EC World and Dasin Retail paints a negative picture on China S Reits in general.

Furthermore, unlike Reits with Singapore assets, we are unable to see the assets and we are not familiar with the general development of the area around the China assets. Moreover, consumers in China may have different consumer tastes than us and thus it may be a challenge to properly evaluate a Reit with assets entirely in China.

| F) Sasseur Reit’s Manager CFO – requested to attend an interview at MAS |

Based on the SGX announcement HERE dated 8 Dec 2022, Mr Xie Jianfeng, CFO of the Manager has informed Sasseur Reit’s Manager that the Authorities are conducting an investigation under the Securities and Futures Act of Singapore 2001 and he was requested to attend an interview at the MAS as he appeared to be acquainted with the circumstances of a case being investigated.

Mr Xie has informed the Manager that the investigation relates to Mr Xie’s personal trading of securities which had occurred before Mr Xie became an employee of the Manager.

Although Sasseur Reit’s manager and Sasseur Reit are not under investigation, any negative developments on this front are likely to cast a pallor on Sasseur Reit’s share price.

|

For a more complete picture, refer to analyst reports (Click HERE); SGX website (Click HERE) and Sasseur Reit’s corporate website (Click HERE). Readers can also refer to Money FM 89.3’s excellent and informative interview with Cecilia Tan, CEO, Sasseur Reit (Click the podcast HERE) dated 23 Jun 2023. Readers can also follow Cecilia’s Linkedin posts HERE which can give you insights to China consumers and Sasseur Reit’s outlets.

Readers have to assess their own % invested, risk profile, investment horizon and make your own informed decisions. Everybody is different hence you need to understand and assess yourself. The above is for general information only. For specific advice catering to your specific situation, do consult your financial advisor or banker for more information

Readers who wish to be notified of my write-ups and / or informative emails, can consider signing up at http://ernest15percent.com. However, this reader’s mailing list has a one or two-day lag time as I will (naturally) send information (more information, more emails with more details) to my clients first. For readers who wish to enquire on being my client, they can consider leaving their contacts here http://ernest15percent.com/index.php/about-me/

P.S: I am vested in Sasseur Reit.

Disclaimer

Please refer to the disclaimer HERE