"China Observer" contributed this article to NextInsight

Next week (25 Oct) Anchun International will mark its 12th year of listing on the Mainboard of the Singapore Exchange.

In the last 10 years, Anchun has paid a dividend only once -- in 2020 for its 2019 performance. The dividend was SGD0.026 a share, which was 50% of net profit. Based on my understanding of management’s intentions, in other years it would have liked to pay a dividend if not for the poor business. |

||||||||||||||||

- Business has been poor in the last decade because of an oversupply in China’s fertiliser industry, leading to poor profitability for many of Anchun’s customers.

Hence, the demand for Anchun’s technology and products was subdued as well. Founder and now non-executive director Xie Ding Zhong at SGX auditorium for Anchun's IPO in 2010, with his daughter, Xie Ming, now Non-Independent Non-Executive Chairman.

Founder and now non-executive director Xie Ding Zhong at SGX auditorium for Anchun's IPO in 2010, with his daughter, Xie Ming, now Non-Independent Non-Executive Chairman.

NextInsight file photo.

- Anchun strived to break out of the fertiliser industry and succeeded in 2017 after years of R&D and expansion of usage in its patented technologies. By securing customers outside of the fertiliser industry, it increased its order book from RMB 86.6m (Dec 2017) to RMB 162.1m (June 2022).

- Within the 162.1m orderbook, RMB 137.4m of orders are from non-fertiliser industries. In comparison, in Dec 2017, the order book was almost entirely made up of fertiliser industry customers.

- 1H2022 revenue was RMB 82m. I expect 2H revenue to reach approximately RMB 107m (See Pg 15 of Half yearly results 2022, section 4.5: Transaction price allocated to remaining performance obligation). Assuming no delay in deliveries, FY2022 revenue would be the highest since 2010.

- Cash and cash equivalents increased from RMB 136.6m in 2017 to RMB 165.5m as of 30 June 2022.

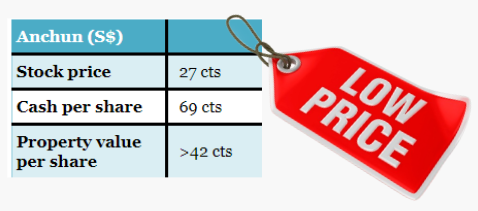

- Current cash levels equate to SGD 0.69 per share, with zero debts. The attraction of the cash and the stock price (around 30 cents) being at a massive discount have to be weighed against the fact that trading has been illiquid.

- Anchun is sitting on a valuable asset – its manufacturing facilities with total building area of 95,000 square meters located in Hunan, Changsha.

- On page 120 of annual report 2021, investment properties carried at RMB 3.7m in books have a fair value of close to RMB 20m and generate rental income of RMB 2.3m.

- A very conservative fair value estimate of the entire manufacturing facilities in Changsha is at least RMB 100m – which is equivalent to SGD 0.42.

- Meanwhile, shares outstanding have been reduced from 50.3m to 47.7m due to share buybacks over the last 5 years. From July 2017 to December 2021, the company bought back more than 2.8m shares, equivalent to 5.5% of total shares outstanding.

- It is likely that the next few years will bring about higher profitability for Anchun’s business. Will the company reward shareholders through higher dividends/more aggressive share buybacks? I certainly hope so.

Anchun’s outstanding innovation and multiple patented technologies and products which focus on energy conservation and pollution reduction are well positioned to meet the market’s needs (Pg 1 of Annual Report 2021, Corporate Profile)

See also: ANCHUN: Investors seek to requisition EGM for special dividend