SAC Capital has put out a non-rated report on Singapore-listed China Shenshan Orchard Holdings, which is China's largest kiwifruit producer.

Excerpts:

Analyst: Peggy Mak

| Established in 2009, Shenshan cultivates and sells kiwifruits in China. Its output accounts for 0.1% of China’s total kiwifruit production of 3 m tonnes in 2019. It develops varieties in-house and owns 6 premium kiwifruit variety rights, holding 83 trademarks and 56 patents. Shenshan (previously Dukang Distillers Holdings Ltd) was listed in July 2021 when baijiu operations were sold back to major shareholder Wang Peng, in return for the kiwifruit operations at a valuation of RMB 1.1 bn. No cash or shares were issued. A new management team came on board. |

About 40% of planted areas are mature acreage. Shenshan operates 9 plantations in Chibi City, Hubei Province, the PRC, with total planted area of 241 hectares. Of these, about 40 are mature acreage (between 5 to 10 years).

The remainder are immature plants of below 4 years.

|

BBG |

DKNG SP |

|

Market cap |

S$25.5m |

|

Price (1 April 2022) |

S$0.32 |

|

52-week range |

S$0.061 – S$0.57 |

|

Target Price |

Non-rated |

|

Shares Outstanding |

79.8m |

|

Free Float |

45.3% |

|

Major Shareholder |

Wang Peng 29.5% |

|

P/BV (12/21) |

0.1x |

|

Net Debt to EBITDA (12/21) |

Net cash |

|

Source: Company data, Bloomberg, SAC Capital |

|

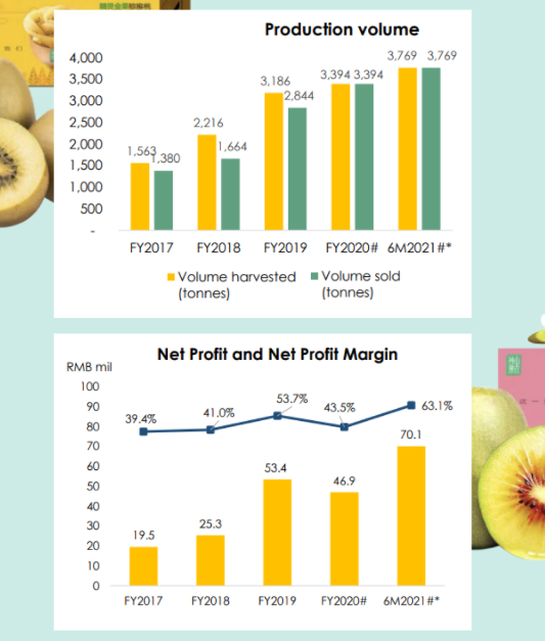

Harvesting of kiwifruits begins after 4 years of cultivation, and harvest takes place every Sep/Oct. It produced 3,769 tonnes in FY 21 at a yield of 40.3 tonnes /mature hectare.

The products are sold in China via wholesalers, distributors and e-commerce retailers.

About 34.6% of total 696 hectares have been planted. The land use rights expire in 2058 and 2059.

This includes a 42 hectare plot of land which it does not yet have valid rights of use, which accounts for ~6% of total acreage and 11-13% of production volume.

Shenshan also holds the rights to 65 000 sqm of industrial land which houses the office and packing facilities.

To raise production output, Shenshan jointly develops farmland with land owners, or engages farmers to provide contract farming.

For instance, it has a non-binding 30-year MOU with Chibi Green Industry Development Investment Co Ltd to develop a 333 hectare land. Chibi Green will provide RMB 150 m investment while Shenshan will develop and operate the plantation.

* Six months ended 31 Dec 2021, with respect to the continuing operations of the Group, being the kiwifruit business. * Six months ended 31 Dec 2021, with respect to the continuing operations of the Group, being the kiwifruit business.Earnings are seasonal. Bulk of sales take place in late 3 Q/early 4 Q. Gross margin has risen steadily to 13.3% from economies of scale with growing mature acreage.  Peggy Mak, analyst.Excluding non-recurring gain on bargain purchase (RMB 10.5 m) and profit from discontinued operations (RMB 34.8 m), the share trades at FY 21 adjusted PE of 3.8 x and EV/EBITDA of 0.7 x. Peggy Mak, analyst.Excluding non-recurring gain on bargain purchase (RMB 10.5 m) and profit from discontinued operations (RMB 34.8 m), the share trades at FY 21 adjusted PE of 3.8 x and EV/EBITDA of 0.7 x.Seeka Ltd, the largest kiwifruit producer in Australia and New Zealand with a 26% market share, trades at 13.6 x and 5.3 x respectively. Both companies generated similar ROIC of 3-4% though Shenshan’s sales were only 8% that of Seeka’s. |

Dukang was placed on SGX watchlist on 4 Dec 2019. Shenshan’s listing status will be in doubt by 4 Dec 2022 if its market cap does not hold above S$40 m on average for a 6-month period, unless SGX grants an extension.