Excerpts from DBS Research report

Analysts: Wei Le CHUNG & Lee Keng LING

| To new all-time highs |

| What’s New • FY20 net profit surges 85% y-o-y to S$97.6m

• Trading at a 51% discount to its peer average of 21.0x • Maintain BUY with a higher TP of S$5.36 |

||||

Investment Thesis:

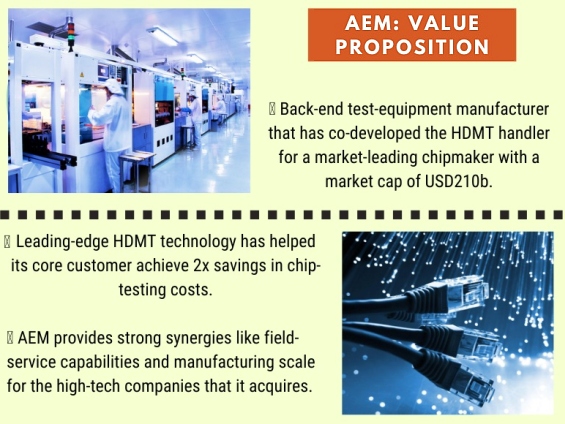

Undemanding valuations for a fundamentally strong company.

AEM is in a strategic position to benefit from its key customer and industry uptrend.

The stock is currently trading at 10.3x FY21F PE, which is at a 51% discount to its peer average of 21.0x.

We are expecting earnings to grow at a CAGR of 12.8% from FY20-23F.

Semiconductor industry momentum remains strong. The World Semiconductor Trade Statistics (WSTS) have raised their forecast of global semiconductor sales by 1.2ppts to 8.4% in 2021, from 6.2% previously.

The US semiconductor equipment billings continues to rise and recorded 29.9% y-o-y increase in January.

Proposed acquisition of CEI will be EPS-accretive, but is not perfectly complementary, in our view. While there is EPS accretion of c.6% on a full-year basis, we think the acquisition does not directly complement AEM’s business nor does it help in advancing its technological capabilities.

| Valuation: Maintain BUY and with a higher TP of S$5.36. We lift our FY21F/22F earnings by 8%/22% on the back of continued strong momentum in the industry and the inclusion of CEI’s financials. Our TP is pegged to 13.7x FY21F earnings (previous peak in FY18). |

Where we differ:

We are more optimistic on AEM’s earnings and the continued strong momentum in the industry.

Key Risks to Our View:

Single-customer concentration risk, geopolitical events, protraction of the COVID-19 pandemic, and FX risk.