Excerpts from UOB KH report

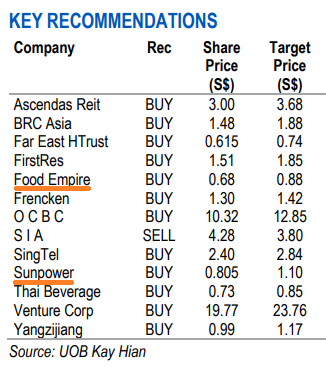

| Alpha Picks: Strong Outperformance In Dec 20; Add Sunpower And Food Empire  Our portfolio gained 7.3% mom in Dec 20, outperforming the FSSTI’s +1.3% mom. Our portfolio gained 7.3% mom in Dec 20, outperforming the FSSTI’s +1.3% mom. For 2020, our portfolio also outperformed, rising 3.9% yoy, significantly better than the FSSTI’s 11.8% loss. For Jan 20, we switch out of Wilmar for First Resources, add Sunpower and Food Empire, and take profit on Nanofilm and Japfa. |

WHAT’S NEW

• Robust performance in Dec 20. Our portfolio rose 7.3% mom in Dec 20, outperforming the FSSTI’s moderate gain of 1.3% mom.

Close to half of the stocks in our portfolio recorded gains of more than 8% mom, led by Nanofilm (+37.5% mom), Frencken (+16.8% mom), Japfa (+15.5% mom) and Wilmar (+10.5% mom).

SingTel (-3.3%) and Far East Hospitality Trust (-2.4% mom) underperformed.  A Sunpower project that supplies steam to an industrial park in Quanjiao.

A Sunpower project that supplies steam to an industrial park in Quanjiao.

Photo: Company

• Add Sunpower and Food Empire. We add Sunpower to our portfolio, given the recent announcement of the sale of its M&S business at an attractive 12x 2019 PE, or twice the 5-7x ascribed by the street and represents 50% of its market cap.

Post sale, the group intends to pay out a special dividend of S$0.2359/share, split into two tranches, translating into an attractive dividend yield of 29%.

For Food Empire, its share buyback amounting to S$1.6m (0.4% of market cap) in 4Q20 and Jan 21 underlines management’s confidence in its business outlook and signals potentially strong 4Q20 results, in our view.

Furthermore, the group trades at a compelling 9.8x 2021F PE.

• Switching out of Wilmar for First Resources. Given Wilmar’s strong share price performance, we switch it out of our portfolio and add First Resources, given that it is a direct beneficiary of higher CPO prices.

We upgraded its 2021 CPO price forecast by 15% to RM3,000/tonne.

• Take profit on Nanofilm and Japfa to lock in gains of 41.4% and 37.5% respectively since their inception into our portfolio.

• Disposal of M&S business. Sunpower Group (Sunpower) is selling its manufacturing & services (M&S) business for Rmb2.29b. The sale price translates into 12.2x 2019 PE and represents close to 50% of Sunpower’s current market cap. We deem the deal as attractive, at a valuation more than twice the 5-7x ascribed by the street. Furthermore, the disposal of the order-driven M&S business will leave investors with the remaining power-producing-related green investments (GI) business, which offers greater revenue visibility and certainty. • Special dividend proposed post-sale. Sunpower intends to pay out a special dividend amounting to Rmb1.34b, or S$0.2359/share, split into two tranches. After which, the remaining amount will also be used to repay payables due from the GI business to the M&S business of Rmb130m, as well as Rmb551m earmarked for existing GI projects and working capital. • Redirects strategic focus to successful GI business. The GI business has significantly more potential to deliver long-term sustainable benefits to the group due to its proven capacity to deliver sizeable recurring income and cash flow. Unlike M&S which is an inherently cyclical, order book-driven business that requires high working capital, GI has the ability to generate recurring cash flow that is sustainable over the long term. This is due to:

• Events: a) Faster-than-expected ramp-up of GI projects; b) more EPS-accretive acquisitions. • Timeline: 3-6 months. |

• Daily share buy-back underlines confidence in business outlook. Since the start of the buy-back mandate on 23 Apr 20, 2,761,000 shares have been purchased, forming 0.5% of its outstanding shares.  Promoting the best-selling Cafe Pho in Vietnam. Photo: CompanyThis was mainly carried out in 4Q20 and Jan 20 where FEH bought back a total of around 2.5m shares for about S$1.6m, potentially signalling a strong set of results for 4Q20 and confidence in its business outlook in 2021. Promoting the best-selling Cafe Pho in Vietnam. Photo: CompanyThis was mainly carried out in 4Q20 and Jan 20 where FEH bought back a total of around 2.5m shares for about S$1.6m, potentially signalling a strong set of results for 4Q20 and confidence in its business outlook in 2021.• Compelling valuation. Food Empire trades at an undemanding 9.8x 2021F PE, a significant discount to peers’ average of 20x 2021F PE despite its growing presence in the Vietnam market and leading position in its core markets in Eastern Europe. • Resilient product offerings and strong brand equity. Given the low prices, relatively inelastic and consumer-staple nature of its products, Food Empire is likely to be more resilient and sheltered from an economic slowdown, in our view. Additionally, we highlight that in spite of the weaker ruble against the US dollar, the group has managed to mitigate some of the adverse impact on bottom-line through gradual increases in ASP and cost cuts. We are encouraged by the group’s core earnings (excluding forex) growth of 11.2% yoy in 9M20 despite stringent lockdowns in 2Q20. We believe this is a testament to its strong brand equity in its core markets that has been developed over many years. Share Price Catalysts • Events: Stronger-than-expected recovery in volume consumption and improvement in operating leverage. • Timeline: 3-6 months. |

Full report here.