Excerpts from RHB report

Analysts: Jarick Seet & Lee Cai Ling

We visited GSS’ Batam factory and came away quite positive on the company’s outlook. We understand that it is currently operating at >80% utilisation and has earmarked another bigger site to shift to in 2019.

We think that the current weakness represents a good opportunity to accumulate at lower levels. Maintain BUY with a SOP-based SGD0.25 TP (47% upside). |

||||

Watch 2-minute video of visit -->

GSS Energy’s (GSS) high precision engineering with Japanese roots for excellence. GSS was formally set up by the Japanese, and hence its focus and expertise lie in high precision engineering (PE) capabilities, accompanied with high quality standards.

This has enabled the company to secure several blue chip names like Phillip, Panasonic as well as being the only listed SGX manufacturer to have Lego as a customer, whom we know to have very high standards. A majority of their machines are also from European and Japanese brand names.

New factory earmarked – robust growth from existing and new customers. Management revealed that the demand from its existing customers like Phillips and Lego has stayed strong, with orders growing 10-20% YoY.

GSS has also been engaged in ongoing testing with a new customer in the consumer space, and expects to start full-scale production by 1H18 (this could boost the PE division’s topline additionally by 15-20% in FY18F).

Improvising on automation to reduce cuts and increase yields. We understand that GSS has its own engineering, team which focuses on automating some of the labour intensive processes.

This would be done by designing and customising some of the machines to better suit its needs, including writing its own software. That has driven down the total number of workers despite revenue increasing YoY.

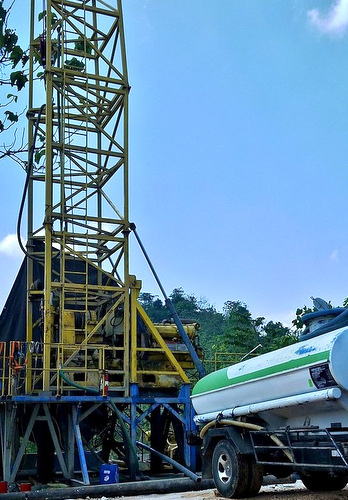

GSS Energy will start producing oil in Indonesia in 1H18. Photo: CompanyProxy to rising oil prices. On 13 Dec 2017, GSS made a hydrocarbon discovery in its Trembul operating area. Management has stated that it expects production of gas to commence in 4Q18. GSS Energy will start producing oil in Indonesia in 1H18. Photo: CompanyProxy to rising oil prices. On 13 Dec 2017, GSS made a hydrocarbon discovery in its Trembul operating area. Management has stated that it expects production of gas to commence in 4Q18. The company is re-entering a makeover well and we expect it to start producing 100-200 bbls of oil a day by 1H18 – and to enjoy better margins and profitability if oil prices continue to increase (an ongoing trend for the past few weeks). Brent crude oil has since hit USD70/bbl compared to the USD60/bbl we use in our forecasts. |

Twin engines point to a positive outlook - Maintain BUY. With a positive outlook ahead affirmed by its recently implemented dividend policy, we think GSS is currently at an inflection point.

At its current share price level, the stock is significantly undervalued. It also provides a unique opportunity for investors to ride on the manufacturing boom and the oil price recovery. We think that the current weakness represents a good opportunity to accumulate at lower levels. Maintain BUY with a SOP-based SGD0.25 TP (47% upside).

Full report here.