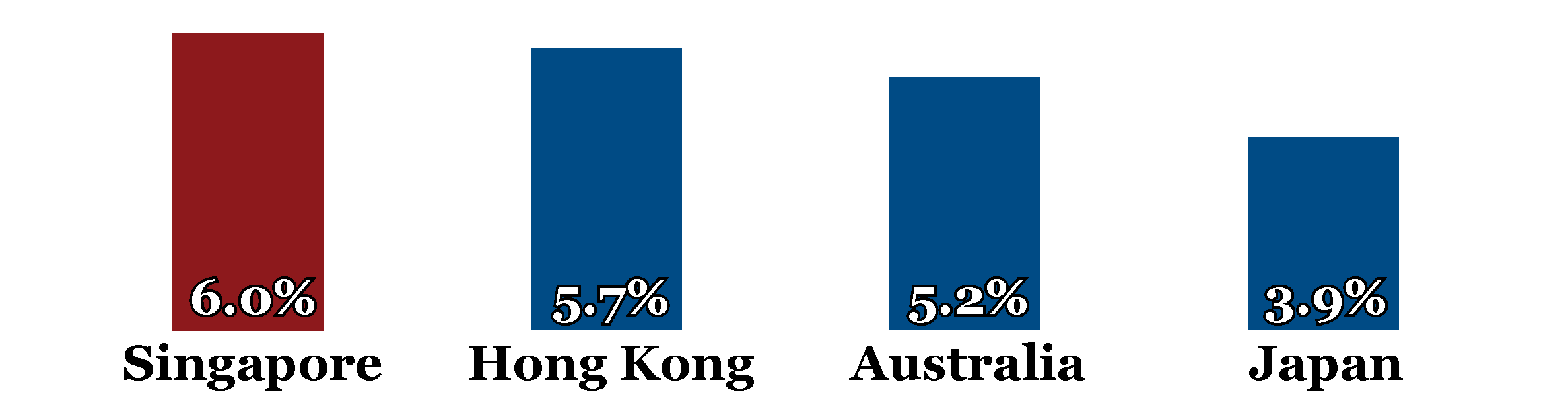

Jeffrey Lee, Phillip Capital Management MD & CIO (left) and Gerard Lee, Lion Global Investors CEO, are joining forces for the first time -- to provide economies of scale for investors through the Lion-Phillip S-REIT ETF. Jeffrey Lee, Phillip Capital Management MD & CIO (left) and Gerard Lee, Lion Global Investors CEO, are joining forces for the first time -- to provide economies of scale for investors through the Lion-Phillip S-REIT ETF.(Photo: Ngo Yit Sung) Demand for REITS is on the rise because a low interest rate environment is now the new normal. Secondly, an ageing population means increasing demand for regular income from an investment portfolio is also contributing to REIT demand. |

REIT value proposition

Real estate prices and rents tend to rise at rates that track or exceed inflation. However, direct real estate ownership has drawbacks such as concentration risk, illiquidity, and management costs.

Retail investors who wish to invest in real estate and avoid these drawbacks often find REITS to be the more viable investment option.

|

|

More and more investors have gone passive. Over the last 15 years or so, passive investing through ETFs has gained a lot more traction.

More and more investors have gone passive. Over the last 15 years or so, passive investing through ETFs has gained a lot more traction.Investing in a REIT offers the following investment edge which would otherwise be the exclusive turf of institutions.

- Access real estate investments in physical assets, and not only in the shares of a listed property developer.

- Access a large scale diversified portfolio of physical real estate.

- When the physical real estate assets increase in market value, or if the REIT makes an accretive acquisition, investors benefit from gains in the REIT market value.

1.) Bugis Junction is one of 16 shopping malls in Singapore owned by CapitaLand Mall Trust.

1.) Bugis Junction is one of 16 shopping malls in Singapore owned by CapitaLand Mall Trust.

2.) Suntec City Convention Centre is part of 4 properties in Singapore and 3 in Australia owned by Suntec REIT.

3.) 8 Chifley Square, Sydney is one of the 9 premium office assets in Singapore and Australia owned by Keppel REIT.

4.) Capital Tower is one of 10 properties in Singapore's central area and next to MRT stations owned by CapitaLand Commercial Trust.

|

The Morningstar® Singapore REIT Yield Focus IndexSM is one of Morningstar’s strategic beta indexes. Security weights (capped at 10% each) are adjusted on the basis of their composite scores for the following factors.

Financial Health Morningstar uses option pricing theory to rank risk of financial distress among peers. Dividend Yield |

||||||||||||||||

Morningstar® Singapore REIT Yield Focus IndexSM

| Index Constituent | Weighting | |

| 1 | CapitaLand Mall Trust | 10.76% |

| 2 | CapitaLand Commercial Trust | 10.25% |

| 3 | Suntec REIT | 9.89% |

| 4 | Mapletree Commercial Trust | 8.98% |

| 5 | Keppel REIT | 8.54% |

| 6 | Ascendas REIT | 8.02% |

| 7 | Mapletree Industrial Trust | 7.64% |

| 8 | Mapletree Logistics Trust | 5.52% |

| 9 | Ascott Residence Trust | 4.54% |

| 10 | Mapletree Greater China Commercial Trust | 3.55% |

| 11 | CDL Hospitality Trusts | 3.50% |

| 12 | Starhill Global REIT | 3.44% |

| 13 | Frasers Commercial Trust | 2.35% |

| 14 | Parkway Life REIT | 2.34% |

| 15 | Frasers Centrepoint Trust | 1.97% |

| 16 | Keppel DC REIT | 1.71% |

| 17 | OUE Hospitality Trust | 1.42% |

| 18 | CapitaLand Retail China Trust | 1.26% |

| 19 | Lippo Malls Indonesia Retail Trust | 1.12% |

| 20 | Frasers Logistics & Industrial Trust | 0.88% |

| 21 | First REIT | 0.86% |

| 22 | Far East Hospitality Trust | 0.76% |

| 23 | Frasers Hospitality Trust | 0.70% |

Data: Morningstar Research (as at 31 August 2017)

For the IPO prospectus, click here.