Shareholders of AEM Holdings should find interesting certain content released today regarding AEM's peer, Cohu Inc, which is listed on Nasdaq.

1). Today (Sept 19), Cohu was upgraded by Needham & Company from Hold to Buy with a US$24 price target.

What's notable is that this upgrade came after Cohu had risen about 67% in the year-to-date. Cohu closed recently at US$23.27.

|

|

AEM |

Cohu |

|

Stock price |

S$2.37 |

US$23.27 |

|

PE (2017F) |

7.7 |

15.1 |

|

Target price |

$3.34 |

US$24 |

|

Market cap |

S$154 m |

US$651 m |

2. Today (Sept 19), Cohu published an investor presentation on its 1H2017 results.

Page 12 of the presentation gave an analysts' consensus estimate for Cohu's full-year 2017 earnings per share: US$1.54.

That translates into a PE of 15.1 based on a recent share price of US$23.27.

On that basis, Cohu is trading at about twice as high a valuation as AEM.

AEM currently trades at $2.37, or a PE of 7.7X, based on CIMB's forecast of 31 cents a share in earnings for 2017.

In terms of market cap, Cohu is about 5.7X bigger at US$651 million while AEM's market cap is S$154 million (or US$114 million).

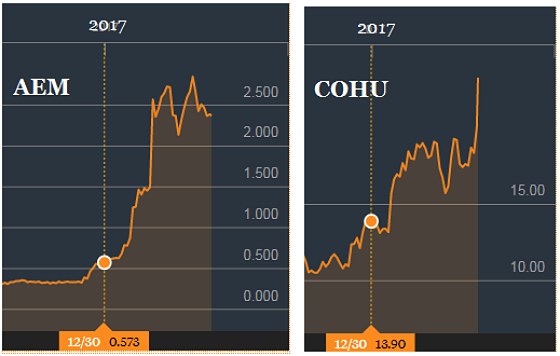

In terms of stock performance, AEM has done a lot better, as the market recognised its first year of ramp-up in production of its new test handler equipment for a global chip company. AEM: Has shot up 313% in the year to date, while Cohu, 67%.

AEM: Has shot up 313% in the year to date, while Cohu, 67%.

Charts: Bloomberg.

|

|