Excerpts from analyst's report

CIMB analysts: William Tng, CFA & Ngoh Yi Sin

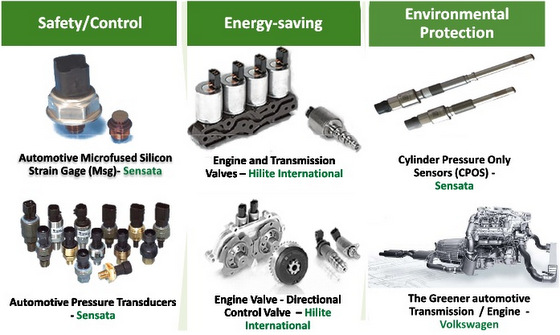

Rise of the Sensor Age ■ Key manufacturer of sensors and engine parts to established, tier-1 clientele such as Sensata Technologies, Hilite International and Measurement Specialties. ■ It is poised to ride two secular growth trends: 1) the advent of ‘smart’ cars which usually use more sensors, and 2) stronger awareness of environmental protection and efficiency ■ Gross margins expected to improve from 26.6% in FY14 to a sustainable level of 30.5% in FY17. ■ Projected dividend yield of 5.0-6.5% in FY15-17 ■ Potential re-rating catalysts include extension into industrial sensor applications and expansion of its premier customer base. |

Initiate coverage with Add and DCF-based target price of S$0.93

Innovalues is a precision metal component supplier to Sensata, a Tier-1 automotive component supplier whose key clients span the likes of GM, Volkswagen, BMW, Mercedes and Honda. We expect higher order volume and improved margins to drive FY15-17 EPS growth of 43%/20%/11% respectively.

Our DCF-derived target price of S$0.93 (WACC: 12.9%) implies a CY16 P/E multiple of 11.1x, which is at 17% discount to its major customer, Sensata’s 13.4x and on par with the overall sector average.

Beneficiary of automotive and sensor market growth

IHS Automotive projects a 5-year CAGR of 4.2% for global automotive production to above 100m in 2017. The CAGR forecasted for auto sensors is more impressive at 9.7%, aided by changing driving trends and tighter regulatory standards for safety, environmental protection and efficiency.

Better, sustainable margins

"Potential re-rating catalysts "Potential re-rating catalystsInnovalues is in talks with both existing and new automotive customers for new product orders which we expect to contribute more significantly in FY17 and have not factored into our forecasts yet. Should this materialise sooner than expected, it would likely be a near-term catalyst. The longer-term catalyst would be expansion beyond the auto segment into industrial sensor applications." -- William Tng, CFA (photo) |

Innovalues has seen a remarkable surge in gross margin from 10.4% in FY09 to 26.6% in FY14, thanks to a more favourable sales mix and enhanced operational efficiency. This has also positively impacted the bottomline, resulting in FY14 core EPS growth of 81%.

With a pipeline of initiatives aimed at reducing labour costs and OA machinery being almost fully depreciated, we expect margins to sustain, if not improve to 30.5% in FY17.

More perks and some risks

As the business generates more cash with little debt and capex, we see a dividend payout of 50% of free cashflow translating into 5.0-6.5% dividend yield in FY15-17. Weaker oil prices and currencies like ringgit and baht could boost the company’s earnings as over 90% of revenue is in US$ vs. c.30% of costs. We estimate that every 1% gain in US$/S$ would add 0.3% pts to gross margins. Key risk is order pushback.