Excerpts from analysts' report

Maybank Kim Eng analysts: Joshua Tan and Derrick Heng, CFA

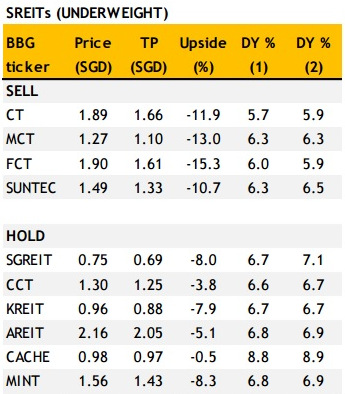

Still in a De-rating Phase Still in a De-rating Phase » Globally, REITs de-rate during times of economic/financial uncertainty, SREITs are no exception. » Only halfway through this de-rating, if history is a guide. » Downgrade Suntec, MCT, FCT to SELL. Maintain CMT at SELL. |

What’s New  We initiated SREITs at UW in Mar 2015, warning of oversupply amid a weak economic backdrop, combined with lofty valuations and tight spreads with benchmark rates, leaving REIT prices vulnerable.

We initiated SREITs at UW in Mar 2015, warning of oversupply amid a weak economic backdrop, combined with lofty valuations and tight spreads with benchmark rates, leaving REIT prices vulnerable.

SREITs have since fallen 12% YTD. This picture has not changed and economic risks are rising. We believe more downside is probable (c.9%) as SREITs traditionally have de-rated in periods of economic /financial market risk.

We reiterate UW with TPs reduced c.23% as we shift to a yield-targeting framework from DDM, in order to reflect the market period we are in. We downgrade Suntec, MCT and FCT to SELL, and downgrade MIT, SGREIT, KREIT and Cache to HOLD. Maintain SELL on CMT.

Only halfway through this de-rating

Globally, REITs de-rate during economic/financial uncertainty, SREITs no exception. We examine three periods of de-rating (2007, 2011 and 2015), and find commonality in rising risks to growth and tightening credit conditions. Balance sheets were sound in all three periods. On top of all this, 2015 has the added pressure of rising interest cost, USD strength eating into SGD returns, and oversupply of space, none of which were present in 2007 and 2011.

"Most negative on Retail. We have grown more bearish regarding demand and rising competition. We expect rents to fall 1% pa in 2015-16 which flattens rent reversions and cuts DPUs by c.3.7%. "Most negative on Retail. We have grown more bearish regarding demand and rising competition. We expect rents to fall 1% pa in 2015-16 which flattens rent reversions and cuts DPUs by c.3.7%. "CMT has traded from -1SD to cycle mean; we expect it to complete the move to +1SD, arriving at a target yield of 6.75%. We price FCT, MCT, and Starhill off CMT with target yields of 7%/7.25%/7.75%." -- Joshua Tan (photo) and Derrick Heng, CFA |

There are more reasons for SREITs to de-rate now than before. SREIT yields have climbed 9% YTD, compared to when they climbed 18% and 19% in 2007 and 2011, implying that we are only half way through this de-rating.

Neutral Office. Economy is slowing and supply will be 3x annual demand in 2016. We expect rents to drop 1%/10%/3% in 2015-17, which results in DPU cuts of c.9%. CCT has de-rated halfway between -1SD and cycle mean, and we expect it to complete the move to mean of 7%. We price KREIT and Suntec off CCT at 7.25%.

Least negative on Industrial. Light at the end of the oversupply tunnel which will finish in 2016. Still, we expect industrial rents to decline 1-2% pa 2015-16 on a weak economy which results in DPU cuts of c.1.7%. Areit has de-rated halfway between -1SD and cycle mean, we expect it to complete the move to cycle mean of 7.25%. We price MIT and Cache off Areit at 7.5% and 9% respectively.

Full report here.