A few dozen investors went to Powermatic Data's recent FY15 AGM.

A few dozen investors went to Powermatic Data's recent FY15 AGM.

Tay Jun HaoI attended the AGM of Powermatic last week. It's not a well-known company but has a small following among the value investing community.

Tay Jun HaoI attended the AGM of Powermatic last week. It's not a well-known company but has a small following among the value investing community.

They operate in a tough industry – and have done as well as anyone could have done in a similar situation. They’ve had 9 straight years of profits, and have paid dividends for the last 8 years, which is impressive by my standards for a company listed on the SGX.

I had a chat with management after the AGM. They struck me as being honest, down-to-earth people with an understanding of the current situation that the company faces. They have a vested interest in seeing the company succeed and turn its fortunes, with Dr Chen Mun (Chairman & CEO) & Ms Ang Bee Yan (executive director) owning a total of 64% of the shares.

So what makes Powermatic interesting?

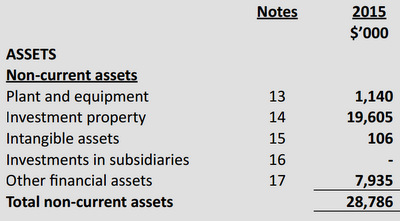

What really strikes me is that Powermatic trades at 0.7x book value. There are many companies that trade at a huge discount to their book value, but plenty of them have assets which are hard to value (intangibles, property, plant and equipment specific to their industry etc).

Powermatic, on the other hand, has a significant portion of its book value in current assets, and a freehold investment property that is stated at $18.6 million.

Footnote details their investment property at 7,9 Harrison Road. Read deeper, and you will see that the property is in fact worth significantly more based on an independent valuation by Knight Frank, and was worth $35 million at the 31st of March 2014.

In other words, Powermatic really trades at 0.5x its book value.

More importantly, the property is freehold and not leasehold, making it all the more valuable. Rusmin Ang from the Fifth Person was kind enough to send me an interesting article on freehold industrial property, which you can check out here.

Here’s the relevant bit:

“The freehold property is a “rare commodity for an industrial site as most buildings released by JTC are on a 20-year lease”, said Ms Christina Sim, the director of investment (capital markets) at Cushman & Wakefield.”

Diving Deeper Into The Balance Sheet

Diving Deeper Into The Balance Sheet

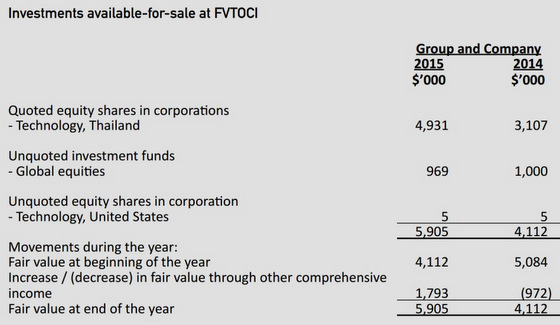

I was quite curious about the make-up of the Thailand portfolio, but unfortunately wasn’t able to get more information on it. Mr Yee Lat Shing, one of the directors (who seems like a seasoned investor himself from his comments), has said that the equities are reasonably priced, and offer an attractive return going forward.

Still, I have my reservations given the considerable run-up in price of close to 60% in a year, and I wish the board had been more forthcoming about the portfolio.

A Closer Look at Remuneration Levels

A glance at their remuneration (below $250,000 a year) reveals that they are, by comparison, lowly paid compared to most boards in Singapore, with most of their remuneration coming in by way of dividends. This is an exceedingly fair arrangement if you compare it to most other listed companies in a similar position, with management taking ridiculous salaries despite the business going downhill (a story for another day).

Conclusion:

Part 1 concludes some of the “hidden value” that lies in Powermatic, and some points that I noted while running through its Annual Report. The next post will cover what I think Powermatic is worth, and why it's a compelling investment opportunity.

What is Powermatic worth?

I primarily think that companies can be valued in two ways: based on cash flows in the future discounted to the present, or based on what a company has. An analogy is a household who has bought a property, car and paid off all its debts with some cash in the bank account. There are two parts to it, the future income stream, of which you can get a good feel based on their previous performance and work history, and what they currently own.

Their equity (total assets – total liabilities) act in the same way the “liquidation value” of a company is. A comment I hear often is that the “value” of these companies can only be realized if they liquidate… but in my experience this is not the case. Very few companies actually undergo liquidation, and there are a variety of ways for “value” to be realised outside of liquidation. Powermatic's investment property @ 7,9, Harrison Road: It is the “Hidden Value” in Powermatic. Photo: Google Maps

Powermatic's investment property @ 7,9, Harrison Road: It is the “Hidden Value” in Powermatic. Photo: Google Maps

Base Value of Powermatic

This is where Powermatic strikes me as being a compelling investment opportunity. Even on a conservative appraisal of their assets, the liquidation value of Powermatic comes close to $40 – $50 million, against a market capitalization at $30+ million. There is no reason for a company of such a track record to trade at such a discount. You could literally buy out Powermatic today at its current price for its investment property – and receive its business and other assets net liabilities for free.

I look at it as buying $1 for 50 cents. The kicker in my view is that it's like buying a REIT – since Powermatic pays a dividend yield of 5.35% at today’s price, and has done so for the last 8 years consistently. Management has a vested interest to keep this payout, with them owning 64% of outstanding shares.

The biggest differentiation with a REIT is that, at this point, Powermatic has not engaged in any borrowings. I pressed the point to management, and suggested they engage in significant share buybacks as one of the resolutions to be passed was a buyback mandate for up to 10% of their outstanding shares. After all, who knows the business best than management themselves… and they are well aware of the gross mismatch between price and value.

Some concluding thoughts:

Howard Marks once said that in investing, take care of the downside and the upside will take care of itself. Powermatic has something which I look for in my investments – an asymmetrical risk reward payout.

The worst case scenario provides an attractive return, and we get a free option on management turning around their business. The consistent 5% + dividend yield makes it all the more compelling.

Time is on my side too, as the value of the freehold property appreciates as the years go by. The current dividend is very much sustainable (costing the company $1.74 million per annum), and management has multiple ways to create value going forward.

Disclosure: The author is long Powermatic.

This article was recently published on The Asia Report, and is republished with permission.