Excerpts from analyst's report

|

We initiate coverage on AP Oil, a Singapore‐based producer of lubricants and specialty chemicals. |

Solid management befitting of a larger entity. Assessing management quality is often overlooked in the investment decision making process. We feel that the team at AP Oil (despite being a small company) stands out sufficiently amongst other SG‐listed companies. We also believe AP Oil’s newly‐appointed CEO, who has been with the group since 2006, has proven his capabilities and is the right man to take the company to greater heights.

Stable core operations. Given the cyclicality of the sector, where it is common for companies to make losses during down cycles, we find it remarkable that AP Oil had managed to remain profitable since 2006 (2005 was the only loss making year since its IPO in 2001). AP Oil’s group revenue has been on an uptrend since 2007 and has doubled its earnings to S$5m since 2008. Overall, AP Oil looks on pace to grow at rate of about 6%. Earnings accretive acquisitions should add to growth and propel valuations.

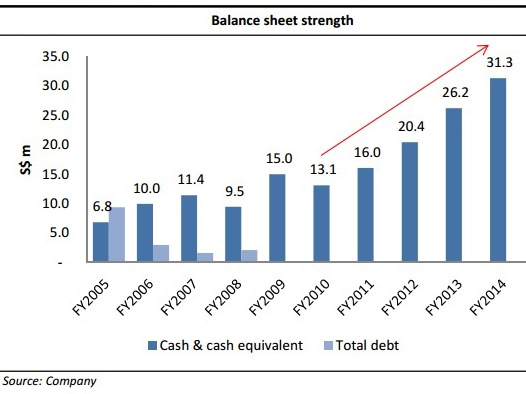

The stage is set for acquisitions. AP Oil has made good acquisitions over the years and had successfully integrated them into the group. We think the conditions are ripe for AP Oil to make more acquisitions in the next one to two years, given 1) its record net cash level of S$31.3m, which opens up more options to the company, 2) Strong credit, which allows it to make leveraged acquisitions, 3) Favorable market conditions for more reasonably‐ priced targets.

CHEAP! With potential catalyst. Trading at just 8.1x FY15F P/E (2.0x ex‐ cash), FY15F P/B at 0.8x and 1.6x FY15F EV/EBITDA, with S$0.19 of net cash per share (out of share price of S$0.25), AP Oil already looks like a delicious bargain. However, stocks can remain cheap without catalysts. Investors can look to potential acquisitions as stock price catalysts. Share price will also be driven higher in the event of a dividend hike. Our target price of S$0.37 is pegged at 12x FY15F P/E, which is a 43% discount to its larger peer, Fuchs.