Excerpts from analyst's report

|

|

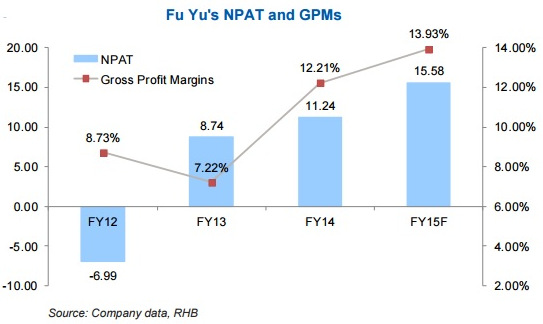

» A robust FY15 ahead. We believe that FY15 could be a record year for Fu Yu, with NPAT levels not seen since FY04. This ought to be accompanied by an approximately 39% YoY NPAT growth for FY15, with margins recovery on cost-cutting, restructuring efforts and projects with better margins.

In addition, the pick-up in business in Singapore and China could also contribute positively to earnings. We also understand that Fu Yu is now in a better position to take up customers or projects with better margins when compared to the past.

» Margins escalation in FY15. We expect Fu Yu’s gross margins to improve significantly to a conservative 13.9% in FY15 from 12.2% in FY14.

As shown in 1Q15, which further substantiates our view, gross margins have actually improved to 14.8% YoY from 8.9%. Going forward, we believe projects with better margins from its precision injection moulding and tooling segments, and the increase in automated processes, will continue to contribute positively to gross margins.

» Capital reduction to allow maiden dividend since FY10 could lead to a 7.1% FY15 yield. From FY11 onwards, Fu Yu did not distribute any dividends due to accumulated losses at the Singapore company level.

With the capital reduction exercise soon to be completed, accompanied by 0.5 cents/share payout, this problem ought to be solved and we expect the company to just pay out a conservative 30% of its NPA, implying an approximately 7.1% yield for FY15.

| » Initiate coverage with BUY and DCF-backed TP of SGD0.30 (TG: 0%, WACC: 12%). This represents c. 88% upside. Fu Yu, with a high potential maiden dividend yield of +7%, is trading at an undemanding 1.7x FY15F ex-cash P/E with a potential record NPAT for FY15. |

» Key Risks.

Customer concentration risk. Currency risk as approximately 80-90% of Fu Yu’s revenue is denominated in USD, while only 50% of its costs are in USD terms.

A reduction in orders from Malaysia.

Full report here.