|

STRATEGY: We stick to our year-end target of 3,400 for the FSSTI. With an expected upside of only 2%, we remain selective and focus on stock-picking to outperform. STRATEGY: We stick to our year-end target of 3,400 for the FSSTI. With an expected upside of only 2%, we remain selective and focus on stock-picking to outperform.

Valuation-wise, at 15.6x 2014F PE, the market is trading at a 4% discount to its long-term mean of 16.2x.

Therefore, even if valuations mean-revert, upside could be moderate, re-affirming our selective stance.

Investment themes we favour include: a) asset monetisation/M&A, b) energy proxies, c) regional growth plays, and d) easing regulatory environment.

Our top picks in the big-cap space include DBS, OCBC, CapitaLand, Keppel Land, CCT, M1 and Ezion.

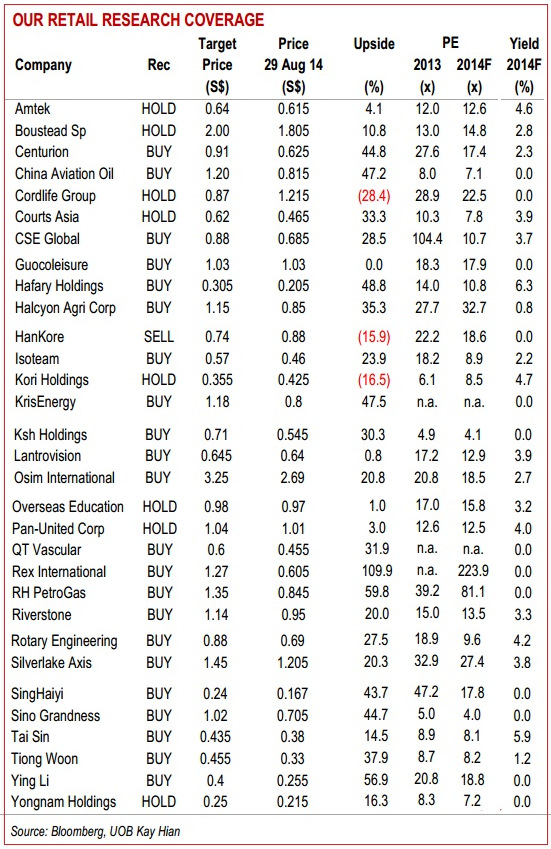

In the mid-cap space, we like Pacific Radiance, Riverstone, Silverlake, Kris Energy and Halcyon.

SELL Tiger Airways, SIA Engineering and Mewah.

|