Excerpts from Deutsche Bank's 12-page report

Analysts: Joe Liew, CFA, and Joshua Lee, CFA

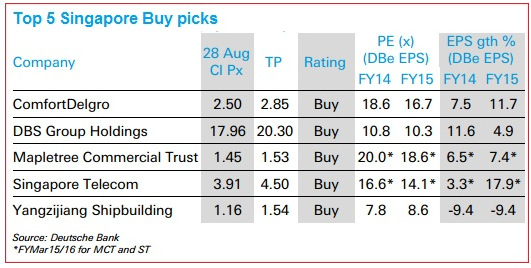

We have reassessed our top picks following a lacklustre 2Q reporting season in Singapore. We add DBS Group and Singapore Telecom (Singtel) to our top 5 Buy picks portfolio and drop Golden Agri and Genting Singapore (GENS).

Deutsche Bank report says: "We continue to be bullish about ComfortDelGro’s focus on overseas growth and further acquisition potential due to its net cash position (SGD 48.1m as at end 1H 2014)." NextInsight file photo.

Deutsche Bank report says: "We continue to be bullish about ComfortDelGro’s focus on overseas growth and further acquisition potential due to its net cash position (SGD 48.1m as at end 1H 2014)." NextInsight file photo.DBS’s fundamentals are better than peers in our opinion because of its deposit franchise, Greater China exposure and lower valuations.

Singtel's market dynamics for its Australian subsidiary, Optus, and associates in Indonesia / India are improving. It also has an attractive forecasted dividend proposition of c.5% for the next 2 FYs.

We turn slightly cautious on GENS because of a continued challenging operating environment in Singapore.

Bottom-up picks should provide alpha as market valuations are not compelling Singapore market valuations do not look compelling: the 2014/15E PE is 14.1x / 12.7x, with EPS growth of 5.4% / 11.4%.

Lacklustre 2QCY14 results, in general, add on to the risk that there might be downgrades to full-year earnings forecasts (see Singapore Strategy: Unexciting 2Q results; possible downside to market earnings forecast, dated 12 August 2014).

We continue to like stocks that provide overseas growth exposure and remain bearish on Singapore property, which makes up c.15% of MSCI Singapore / FSSTI.

|

Fundamental drivers support our top Buy picks

ComfortDelgro: Overseas focus with multiple geographical experience and further acquisition potential should drive growth. SG bus prospects should improve when the bus contracting model reforms slated for 2016 kicks in.

DBS Group: Wealth management niche in HK and SG should drive its earnings momentum. NIM, non-interest income, asset quality and deposit franchise exceed those of peers. Better positioned than peers for an interest rate rise.

Mapletree Commercial Trust: Strong operational momentum in VivoCity, positive reversions on its office portfolio and deep pipeline. FYMar15 dividend yield of 5.3% and DPUs are expected to grow 14% over next two FY.

Singapore Telecom: Better data monetization in the Singapore market. Australia, Indonesia and India market dynamics are improving. Attractive forecasted dividend yield of 4.6%/5.4% for FY15/16 (75% payout ratio).

Yangzijiang Shipbuilding: Capturing market share during current consolidation. USD 5bn order book should allow its yards to remain well utilised through 2016.

In Singapore, we have Sell recommendations on NOL / SIA / SMM.

|