Excerpts from analysts' reports

Macquarie Research says Ezion is going "from strength to strength"

Analyst: Somesh Kumar Agarwal

Event

Ezion reported robust 26% YoY growth in profit (S$ 45.5mn) in its 2Q14 results.

We see robust 42% upside in Ezion’s share price from current levels as the company delivers 37% profit CAGR over 2013-16E, which should lead its PE multiple to compress to 7.1x 2015E and 6.0x 2016E (based on current price). Our estimates for 2015 and 2016 are 7% and 12% ahead of consensus.

Ezion specialises in the development, ownership and chartering of strategic offshore assets and the provision of offshore marine logistics and support services to the offshore oil and gas industries. Photo: annual report

Ezion specialises in the development, ownership and chartering of strategic offshore assets and the provision of offshore marine logistics and support services to the offshore oil and gas industries. Photo: annual report

Looking forward:

19 out of 36 vessels have not contributed to FCF, P&L yet: Less than half of the fleet has accounted for the current revenues and profits. Thus, profit levels are bound to at least double from current levels as these 19 vessels are delivered in the course of next 24 months.

Contracts run until 2022; Cash flows secured: Only 6 of 36 vessels’ contracts are expiring by end-2015E. Most vessels have 5-7 year contracts.

12-month price target: S$3.00 based on a DCF methodology.

Action and recommendation

A value buy with risk-reward strongly in favour: We believe the current share price does not reflect the pace of fleet growth, impending profitability and reduced leverage. We recommend Ezion for long-term value buyers.

Recent story: EZION: Credit Suisse initiates coverage with 'underperform' rating

|

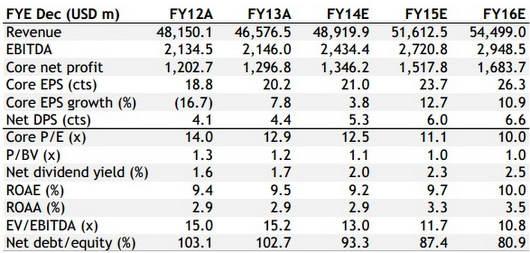

Maybank Kim Eng says Wilmar has "stronger foothold in food chain"

Analyst: Wei Bin

§ Two growth drivers — recovering soybean crushing margins and sugar price rebound — are intact, in our view.

§ YTD acquisitions to diversify revenue sources and strengthen position along the food value chain.

§ Stay invested despite short-term earnings volatility. Maintain BUY and TP of SGD3.94, set at 15x FY14E P/E.

Growth drivers intact

We continue to believe in Wilmar’s long-term earnings recovery. In our view, its two growth drivers — recovering soybean crushing margins in China and a sugar price rebound — are intact. We forecast an EPS CAGR of 11.8% over FY15E-16E, after a muted EPS growth of 3.8% in FY14E.

Investing for the future

Soft commodity prices of sugar, corn and soybean etc., could present golden opportunities for the acquisition of distress assets.

Wilmar has announced several sizeable acquisitions YTD, which would not only further diversify its revenue sources but also strengthen its position along the value chain.

Beyond near-term earnings volatility

We expect short-term earnings to remain volatile. We are looking at a USD185m net profit for 2Q14E, down 15% YoY but up 14% QoQ. But look beyond that for its recovering crushing margins and better sugar prices.

Reiterate BUY with an unchanged TP of SGD3.94, based on 5-year average of 15x FY14E P/E.

|