OSK-DMG: Cordlife has "vast potential for strong earnings growth"

Analysts: Arshath Mohamed & Shekhar Jaiswal

Jeremy Yeh, CEO of Cordlife. NextInsight file photo.We initiate coverage on Cordlife Group “Cordlife” with a SGD1.50 TP which represents a 29% upside and recommend BUY.

Jeremy Yeh, CEO of Cordlife. NextInsight file photo.We initiate coverage on Cordlife Group “Cordlife” with a SGD1.50 TP which represents a 29% upside and recommend BUY. Cordlife stores cord blood, which is being used to treat various diseases. Cordlife’s strong presence in the mature markets of Singapore and Hong Kong, and recently, high-growth countries like India, Indonesia and the Philippines, allows it to tap the rising awareness and adoption of cord blood storage in Asean.

Expanding to growth markets. Having developed a strong presence in mature markets like Singapore and Hong Kong, where the industry penetration rate is 22%, Cordlife is expanding into the India, Indonesia and Philippine markets, where the penetration rates are 0.1-0.2%.

It also has exposure in Malaysia and China through investments in Stemlife (STEM MK, NR) and China Cord Blood Corp (CO US, NR), respectively.

It also has exposure in Malaysia and China through investments in Stemlife (STEM MK, NR) and China Cord Blood Corp (CO US, NR), respectively.

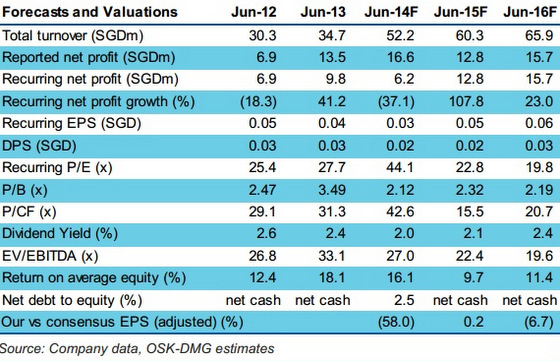

Vast potential for strong earnings growth. We expect earnings to reach a 60% CAGR during FY14F-16F, aided by: i) the ramp-up in high-margin cord tissue storage service business, and ii) rapid growth in three burgeoning markets.

Our 10% annual penetration growth assumption for growth markets is lower than the 20% estimated by an independent consultant, as well as the growth achieved in recent years.

Our 10% annual penetration growth assumption for growth markets is lower than the 20% estimated by an independent consultant, as well as the growth achieved in recent years.

Recurring revenue. Cordlife‟s 21-year deferred payment scheme for its cord blood/tissue storage services translates into a stream of recurring revenue. Customers also have an option to have the cord blood/tissue stored for life after the expiry of their contracts. We remain optimistic that most existing customers may potentially extend their contracts.

A new revenue stream. The company is looking to diversify into diagnostics services in the “mother and child” segment and roll out 1-2 new diagnostics products over the next few years. Given the low margins in the diagnostics services business, any meaningful contribution would depend on volume. We have not factored this into our estimates as yet.

Initiate coverage with BUY. Given the recurring nature of its earnings, we value Cordlife using DCF. From this we arrive at a TP of SGD1.50, after adjusting for its investments in Stemlife and CCBC, as well as its net cash balance

Full report here.

Recent story: CORDLIFE: Analysts expect strong FY2014 growth