|

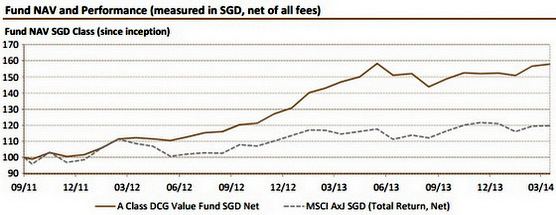

At end March 2014, the portfolio comprised 68 holdings with cash reduced to 9% after the fund manager deployed more cash into a number of new ideas as well as adding to existing positions on share price weakness. |

Here are excerpts from the fund's recent letters to investors:

DKSH Malaysia employs about 3,600 people in a knowledge-based business model and acts as route-to-market specialists to provide market information, leading product and application expertise, marketing, sales and logistics expertise, and state-of-the-art IT. Photo: CompanyEstablished in 1923 in Penang and listed on the Kuala Lumpur Stock Exchange since 1994, DKSH Malaysia (“DKSH (M)”) is a 74%-owned subsidiary of the Zurich-based DKSH Group.

DKSH Malaysia employs about 3,600 people in a knowledge-based business model and acts as route-to-market specialists to provide market information, leading product and application expertise, marketing, sales and logistics expertise, and state-of-the-art IT. Photo: CompanyEstablished in 1923 in Penang and listed on the Kuala Lumpur Stock Exchange since 1994, DKSH Malaysia (“DKSH (M)”) is a 74%-owned subsidiary of the Zurich-based DKSH Group.

The company provides logistic services for consumer and healthcare products and market expansion services (“MES”) for fast moving consumer goods (“FMCG”). It also owns the Famous Amos chocolate cookies chain with 88 stores across Malaysia.

MES entails product feasibility studies, registration, importation, customs clearance, brand and product management, sales, marketing, trade relation management, field marketing and point-of-purchase services, procurement, warehousing, physical distribution, logistic services, invoicing, cash collection and after-sales services. DKSH offers one-stop-shop solutions to clients who look for quick market access, local knowledge and a trustworthy business partner in emerging Asia.

In healthcare distribution, DKSH is head-to-head to its Swiss peer- Zuellig Pharma in both pharmaceutical and medical devices categories.

For healthcare logistic business, DKSH (M) distributes products for more than 69 international and local healthcare companies to over 10,000 customers across doctors’ clinics, retail pharmacies, private hospitals, government hospitals and institutions and selected wholesalers.

While profit margins are thin the company achieves relatively high ROE (above 16% since 2010) as DKSH (M) operates on an asset light, fast asset turnover model, in line with the parent company’s strategy.

Among our seven portfolio building blocks, we place DKSH (M) in the steady growth bucket as we expect growth to be in the high single digit area in the coming years.

Over the past 10 years, sales and earnings before tax and interest (EBIT) have grown at an average rate of 7.9% and 17.9% respectively. In 2013, the company reported top line and core operating profit growing 7.5% and 7.2% year on year (y-o-y), respectively. Revenue from consumer goods was RM2,266.8 million (+9.6% y-o-y), while logistics services contributed RM2,750 million (+5.3% y-o-y) in sales. Famous Amos cookies chain posted RM62 million revenue, a 7.9% y-o-y increase.

When we first came across the idea, DKSH (M) was selling at PER of 5x and was little followed by both the sell and buy sides. Since then, the stock has attracted more investor interest and been re-rated massively to a current PER of 17x on recurring earnings..

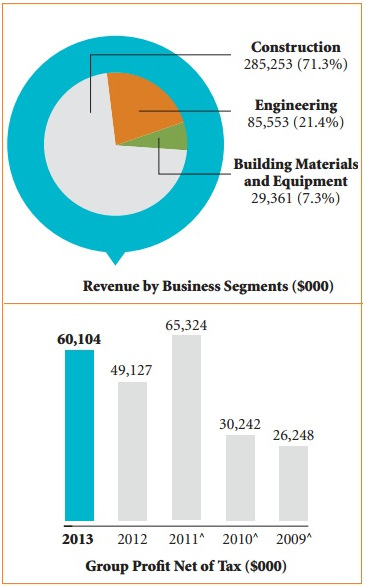

UE E&C, a subsidiary of United Engineers Limited, is a major player in the construction and engineering sector in Singapore. UE E&C has also established a niche for itself as one of the largest construction and M&E service providers in Brunei.

UE E&C, a subsidiary of United Engineers Limited, is a major player in the construction and engineering sector in Singapore. UE E&C has also established a niche for itself as one of the largest construction and M&E service providers in Brunei.In recent years, UE E&C’s construction projects have included profitable middle and upper market high-rise residential housing in Singapore such as the high-end Paterson Suites, and the popular Waterwoods and Watercolours Executive Condominiums.

UE E&C has also performed civil engineering works on high-end purpose built facilities such as the Biopolis and Fusionopolis (science and research hubs in Singapore), and several MRT (rail-based mass transport) stations.

Over the recent few years, profits from UE E&C’s stake in such developments have contributed up to 20% of the company’s total annual profits before tax.

Through another of its subsidiaries, United Engineers (Singapore) Pte Ltd that has strong track record of over 25 years, UE E&C is well established as one of the leading M&E contractors in Singapore, having fitted out many local landmarks including the National Library along Victoria Street, retail buildings in the heart of Singapore’s shopping district such as ION Orchard and Ngee Ann City, and the iconic Marina Bay Sands, one of Singapore’s most expensive buildings.

We invested in UE E&C in 2012 when it was considerably undervalued at only about S$0.60 per share and was providing a dividend yield of over 8%. We invested in UE E&C in 2012 when it was considerably undervalued at only about S$0.60 per share and was providing a dividend yield of over 8%. With over S$121 million in net cash sitting on its balance sheet and a market capitalization of only S$170 million then, the stock was clearly undervalued as the market was pricing the stock on only 2.6x trailing earnings and 0.59x of its book value. We reckoned the cheapness was probably because of the company’s small capitalization and hence was a much neglected stock. The share price had recently appreciated strongly to over S$1.40 on speculation of a potential bid for the company. |

The information and materials contained in or accessed through this website are provided on an "as is" and "as available" basis and are of a general nature which have not been verified, considered or assessed by DCG Captital Pte. Ltd. (“DCG”) in relation to the making of any specific investment, business, financial or commercial decision. Such information and materials are provided for general information only and you should seek professional advice at all times and obtain independent verification of the information and materials contained herein before making any decision based on any such information or materials.

DCG does not warrant the truth, accuracy, adequacy, completeness or reasonableness of the information and materials contained in or accessed through this website and expressly disclaims liability for any errors in, or omissions from, such information and materials. No warranty of any kind, implied, express or statutory (including but not limited to, warranties of title, merchantability, satisfactory quality, non-infringement of third-party intellectual property rights, fitness for a particular purpose and freedom from computer virus and other malicious code), is given in conjunction with such information and materials, or this website in general.

The views expressed are opinions of DCG and are subject to change based on market and other conditions. These views are not intended to be a forecast of future events, a guarantee of future results or investment advice. Nothing in this website constitutes accounting, legal, regulatory, tax or other advice.

Under no circumstances shall DCG be liable regardless of the form of action for any failure of performance, system, server or connection failure, error, omission, interruption, breach of security, computer virus, malicious code, corruption, delay in operation or transmission, transmission error or unavailability of access in connection with your accessing this website and/or using the online services even if DCG had been advised as to the possibility.

In no event shall DCG be liable to you or any other party for any damages, losses, expenses or costs whatsoever (including without limitation, any direct, indirect, special, incidental or consequential damages, loss of profits or loss opportunity) arising in connection with your use of this website, or reliance on any information, materials or online services provided at this website, regardless of the form of action and even if DCG had been advised as to the possibility of such damages.

DCG Capital Pte Ltd is a Registered Fund Management Company as defined in the Securities and Futures Act of Singapore ("SFA"). Accordingly, each client of DCG Capital Pte Ltd must be a qualified investor or accredited investor as defined under the Securities and Futures Act of Singapore (Cap. 289).