Prior to his retirement, Chan Kit Whye worked more than 30 years as Regional Finance Director, Financial Controller and Manager in a multinational specialty chemical business. He has played an active role in CPA (Australia) Singapore Branch, taking up positions in its Continuing Professional Development and Social Committees. Kit Whye is a Fellow of CPA Australia, CA of Institute of Singapore Chartered Accountants and CA of the Malaysian Institute of Accountants. He holds a BBus(Transport) Degree from RMIT, MAcc Degree from Charles Sturt University and MBA from Durham Business School.

Prior to his retirement, Chan Kit Whye worked more than 30 years as Regional Finance Director, Financial Controller and Manager in a multinational specialty chemical business. He has played an active role in CPA (Australia) Singapore Branch, taking up positions in its Continuing Professional Development and Social Committees. Kit Whye is a Fellow of CPA Australia, CA of Institute of Singapore Chartered Accountants and CA of the Malaysian Institute of Accountants. He holds a BBus(Transport) Degree from RMIT, MAcc Degree from Charles Sturt University and MBA from Durham Business School.UOB Kay Hian: Wee Ee Chao has been increasing his stake in UOB Kay Hian recently, and to date holds 23.26% of the company.

Wee Ee Chao, Chairman and MD of UOB-Kay Hian Holdings. Photo: Internet

Wee Ee Chao, Chairman and MD of UOB-Kay Hian Holdings. Photo: InternetUOB itself holds 39.4% of UOB Kay Hian.

Combining both, total holdings have reached 62.7%. Public float, therefore, is about 37.4% or 271 million shares.

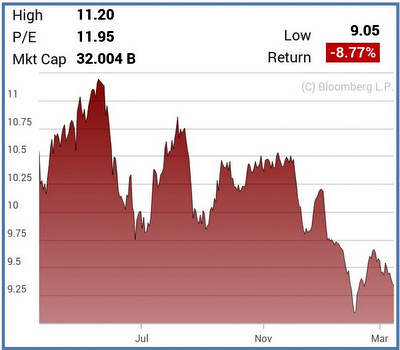

UOB Kay Hian's 2013 profit was spectacular. Profit attributable to shareholders was $93.3 million versus $65.7 million in 2012, or a 42% improvement.

Earnings per share for 2013 was 12.9 cents, 3.8 cents higher than in 2012.

Net Asset Value is $1.58 a share. Dividend declared is up from 4.5 cents a share for 2012 to 6.5 cents a share for 2013.

UOB Kay Hian has continued to acquire more shares in its Thailand subsidiary, and now owns about 70.6% of its subsidiary.

My opinion is that there is a possibility of taking its Thai subsidiary private eventually and that would give UOB Kay Hian more flexibility in managing its Thai operations.

UOB Kay Hian is the only listed brokerage firm on SGX that has not been acquired or taken private.

If there is no need for public funds, there is no reason to keep the company listed, in my opinion.

Kim Eng Securities was acquired by Maybank at a hefty price of $1.79 billion, or $3.10 a share. That was a 36% premium over its stock’s average price over the past 20 days and 1.9 times its book value.

UOB Kay Hian's price-to-book ratio is only 1.05 times and whoever wants to take the company private must at least able to match Maybank's offer to privatise Kim Eng.

OCBC: According to Lianhe Zaobao, OCBC will acquire Wing Hang Bank (WHB) at HK116 per share or HK$35.6b (S$5.8b). OCBC: According to Lianhe Zaobao, OCBC will acquire Wing Hang Bank (WHB) at HK116 per share or HK$35.6b (S$5.8b). However, WHB will be paying cash dividend of HK$21 per share to existing shareholders prior to the acquisition. UOB Kay Hian's observations are as follows: The stated price tag of HK$35.6b (S$5.8b) is lower than our previous expectations of US$5b (S$6.35b). If adjusted for the distribution of HK$21 per share to existing shareholders, the P/B for the acquisition would be 2.34x based on the balance sheet as of Dec 13, which is higher than our previous estimate of 1.91x. The goodwill on OCBC's balance sheet would be higher at S$3,326m, higher than our previous estimate of S$2,943m. The deal may have been restructured to close the gap in pricing. It is rumoured that OCBC wanted to keep the price tag below P/B of 2.0x while shareholders of WHB expected P/B to be at 2.3-2.4x. UOB Kay Hian cautioned that OCBC has not reach a definitive agreement with shareholders of WHB yet. OCBC has not made any official announcement on the potential transaction to acquire WHB. |