Main reference: Story in Sinafinance

CHINA HASN'T WITNESSED a newly-listed enterprise in over half a year.

So what froze new listcos in the first place and what would happen if the floodgates were suddenly reopened?

The stock market watchdog, the China Securities Regulatory Commission (CSRC), has frozen IPOs since October of last year.

In 2010, two years after the collapse of Wall Street, China saw 344 firms raise a record 488 billion yuan as IPOs in either Shanghai or Shenzhen, allowing the PRC to surpass both the US and Hong Kong as the world’s top market for IPO proceeds at the time.

BlueFocus Communication management, including Deputy General Manager Xu Zhiping (second from right) celebrate their A-share IPO as they became the first Chinese PR firm to go public in 2010, a year which saw record IPO proceeds in the PRC.

BlueFocus Communication management, including Deputy General Manager Xu Zhiping (second from right) celebrate their A-share IPO as they became the first Chinese PR firm to go public in 2010, a year which saw record IPO proceeds in the PRC.

Photo: BlueFocusBut the market bit off more than it could chew with liquidity pinched by the influx, causing the benchmark Shanghai Composite Index to slump 14%, giving China the dubious honor of being the worst-performing major Asian stock market from 2010 to present.

The CSRC had seen enough and prohibited new listcos in China over six months ago, until further notice.

The October ban and the tepid sentiment caused IPOs to fall to just 147 in 2012, with proceeds raised plummeting 80% from the record set in 2010 to just under 100 billion yuan.

It’s not for a lack of interest that the gates are temporarily closed because at last count some 765 IPO candidates were waiting impatiently at the threshold, looking for any clues as to when the CSRC might reopen the sluice.

But some have gotten cold feet as around 162 companies have withdrawn their IPO applications since the end of last year at a time when the bourse watchdog ordered both issuers and underwriters to review their filings to help purge fraud from their ranks.

Lately, there has been some activity in the right direction as the CSRC said recently that it would scrutinize nearly three dozen prospectuses selected randomly from over 600 IPO candidates that finished their reviews.

But the market regulator also pushed back the deadline for firms not having submitted their reports to the end of this month – a move which led to market chatter suggesting IPOs might not restart until June at the earlier.

And when China’s IPO market does reopen, it seems quite possible that the overall main board and the representative benchmark Index might not be significantly moved one way or the other.

Instead, when the long freeze is thawed, the CSRC is likely to take tentative baby steps at first, ushering in only small to mid-caps at the outset to allow investors and the overall market to test the waters as it were.

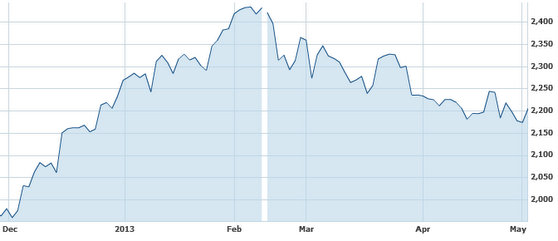

Will a resumption of IPOs put a charge back in China shares? Source: Yahoo Finance

Will a resumption of IPOs put a charge back in China shares? Source: Yahoo Finance

This means that with the resumption of newcomers, the most heavily impacted entities might be the nearly four-year old ChiNext board, often called “China’s Nasdaq,” as well as the SME board itself.

Also, the new national government has been a frequent cheerleader of select high growth potential sectors like renewable energy, hybrid automakers or the country’s highly fragmented pharmaceutical space.

This could mean that the first listcos to break the IPO thaw could come from these sectors.

And given the timid IPO environment of late, the average P/E ratios of newcomers – whenever new listings are re-allowed – might only be in the 10-15x range.

This is a far cry from some of the triple-digit P/Es seen for some IPOs launched on “China’s Nasdaq” at its inception, and could put downside pressure on some existing high P/E ChiNext firms.

See also:

'Chinese Dream' To Wake Up China Shares?