YUANTA: COMTEC SOLAR’S target has 134% upside

Yuanta Securities is raising its recommendation on Comtec Solar Systems Group Ltd (HK: 712) to ‘buy’ from ‘hold’ following a significant valuation decline.

The Hong Kong-listed firm’s 12-month target price was also raised 9% to 2.50 hkd, representing a nearly 134% upside.

“We upgrade to BUY as Comtec’s share price has fallen over 50% since our last report on August 18, and we believe its valuation is now quite attractive,” Yuanta said.

The brokerage also pointed out that China, where Comtec bases its production facilities, has raised the solar power capacity target set in the 12th Five-year Plan another 50% to 15GW.

“In the near term, wafer producers like Comtec will still be under pressure from ASP (average sales price) declines.

"But with the newly-developed demand from China and Japan, and the revival of Europe, we maintain our positive view over the medium and long term,” Yuanta added.

The brokerage called Comtec’s current valuation “compelling.”

“As Comtec is now trading at only 4.0x 2012F EPS, we believe its share price decline is very overdone.”

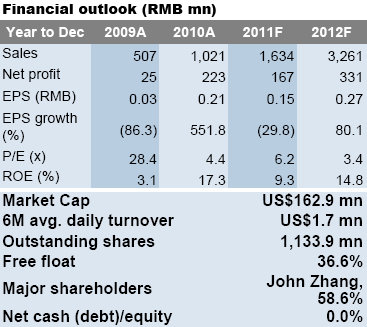

Yuanta said it is raising its 2012 EPS estimates for Comtec to 0.27 yuan from 0.24 as it believes the falling polysilicon prices, potential demand growth from China, and Comtec’s high-end positioning will help it to maintain its gross margin.

“Polysilicon prices -- Comtec’s main upstream cost -- have declined 53% since January. Based on our calculations, although 156mm mono wafer ASP has declined 58% since Jan 2011, the polysilicon price has also declined 53%. Thus, pressure on Comtec’s gross margin is somewhat eased by the polysilicon price decline.”

Yuanta argued that with the company's focus on high-end customers through better quality products like super-mono N-type wafers: “Comtec’s gross margin going forward should be more resilient than other wafer producers.”

See also:

COMTEC’S Sunny 3Q, COMBINE WILL’S Revenue Up 18%, COURAGE MARINE Bolsters Fleet

COMTEC SOLAR, DATANG RENEWABLE POWER: What Analysts Now Say...

UOB: COMTEC SOLAR Initiated With ‘Hold’ Call

UOB Kay Hian has initiated coverage of monocrystalline wafer maker Comtec Solar Systems Group Ltd (HK: 712) with a ‘hold’ recommendation.

Meanwhile, the target price is set at 1.06 hkd. (recent price: 1.12 hkd).

“Comtec Solar is a leading low-cost solar monocrystalline (mono) wafer producer. It is a niche player as its high efficiency super-mono wafer products deviate from mainstream oversupplied multicrystalline technology,” UOB said.

The brokerage added that it expects short-term macroeconomic headwinds to prevail and drag profitability to near breakeven levels in FY2012 for the Hong Kong-listed firm.

“However, we expect Comtec to emerge as an ultimate survivor with a prudent management team and the maintenance of a healthy cash balance through TPG Capital's strategic investment of 780 mln hkd in the first half.”

See also:

COMTEC SOLAR: HK-Listco's 1H Profit Soars 48.1% On Vibrant Wafer Sales

CHINA MINZHONG FOOD, COMTEC SOLAR: What Analysts Now Say...