Translated by Andrew Vanburen from: 電訊盈科: 分手難做嗎? (中文翻譯,請看下麵)

PCCW LTD (HK: 8) has seen its shares now rise to over 3.3 hkd from just 2.7 in less than a month thanks to a spinoff plan and a share buyback by its tycoon Chairman Richard Li, who purchased 2.9 mln shares last week at 3.00 hkd each.

The move is a masterful plan to help reduce friction between shareholders and management of Hong Kong’s top telecom firm.

PCCW provides telecommunications, Internet access, multimedia services and related equipment to Hong Kong’s seven mln citizens, while also investing and developing system integration and technology-related business, infrastructure and properties in Hong Kong and China.

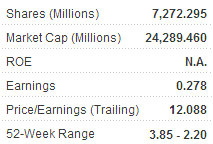

Therefore, a company with such influence, 20,000 employees and a market cap of over 24 bln hkd obviously makes headlines when its high-profile chairman buys back shares, or when management announces plans to spin off and seek a separate listing for its telecom assets via a business trust.

If successful, the move will be the first of its kind for a telecom listco in Hong Kong, resulting in stapled securities, and should help free up both capital and interest in the pared of unit as a pure telecom play as well as go a good distance in mending frayed relations between shareholders and company executives.

The special administrative region’s (SAR) dominant Internet service provider (ISP) and fixed-line firm won authorization from the Hong Kong bourse in early June to list its telecom assets in the form of a business trust, with the plan now requiring approval from both regulators and shareholders to be finalized.

Recent reports have PCCW eyeing some 1.2 bln hkd in proceeds from the listing, with the Hong Kong firm targeting a fourth quarter debut.

If all goes as planned, the spinoff would mark the Hong Kong bourse’s inaugural business trust listing outside of the real estate sector, with PCCW aiming to keep a 55% equity stake in the post-listing assets.

To help grease the skids under the proposed spinoff, Mr. Li pledged to maintain a “stable” dividend payout policy over the next three years, hoping this would help win approval for the deal from minority shareholders.

The spinoff will boost the rights of shareholders of the firm’s newly-listed dedicated telecom business stocks, affording preferential subscription rights to these investors with set-asides held exclusively for them if they wish to boost their stakes.

PCCW’s intention to keep at least a 55% equity stake in the spinoff for at least three years is meant to ensure it can make good on its promises to practice a stable dividend policy over that time period – namely, to maintain payouts at 2010 levels.

PCCW has had a very tumultuous decade, with its valuation dipping at times by 90% from periodic levels.

This has resulted in a large portion of the company’s equity being held longterm by retail investors waiting for a return to more robust share price levels.

Mr. Li said the main rationale for the spinoff was to ensure consistently stable dividends to shareholders at a high level.

However, many shareholders would more likely be happier to see management work on ensuring healthy earnings as well as working to streamline operations and boost the company’s fundamentals.

Relations between minority shareholders and management first soured when PCCW listed its property unit – Pacific Century Premium Developments Ltd (PCPD) – severely diluting shareholder value at the time.

It will be interesting to monitor the progress of PCCW’s spinoff plan this year, and see how cooperative (or cantankerous) shareholder meetings are going forward.

If all goes well, and the company works on its growth strategy into the mix, I think the valuation doldrums for this counter may soon be a thing of the past.

See also:

DMX: Telco Sector Demand Spurred By Technology Replacement

SINOTEL'S PEER IN PRC: GrenTech 2010 Net Triples On WLAN, 3G

電訊盈科: 分手難做嗎?

(文: 古你唔到)

最近電訊盈科(008)提出分拆電訊業務,若然落實,將會以實物形式,分派由商業信託及相關連的電訊控股公司組合而成的合訂股份(stapled securities)。此舉不單在香港股票市場內創下先河,成為香港首間商業信託股,亦為長期受壓的電盈股價,得到增值的空間,間接減少管理層與股東之間的磨擦。

今次電盈的分拆及派送方案,主要向現有股東實物分派部份合訂股份,佔擬分拆的電訊業務股權5%至10%。同時給予股東優先認購權,去認購更多合訂股。繼而安排公開發售,供機構投資者及公眾認購。電盈最終保留電訊業務股權最少55%為時三年,以免重蹈之前提出電訊業務,致原有上市的電盈,面對業務、資產不足以支持上市的尷尬局面。為爭取股東支持,電盈因應出售部份電訊的部份股權引發的主要交易事項,保證未來三年的派息不少於2010年的派息水平。

在當前息口可能進入上升周期,若電盈能夠趕及減持部份電訊業務股權,將有助電盈變相集資。假如如盛傳中電盈可以從出售股份中集資13億美元,按售股佔整體股權比重最多30%計,電訊業務估值最少338億元或以上,未計未來的增值因素,這已經比市值逾225億元的電盈還要高。這甚至已經超過旗下電訊控股公司的股本投資約49.6億元,增值約5.8倍。假如按出售部份業務所得獲利入賬,將谷大電盈的綜合及公司資產負債表中的儲備部份。

由於電盈過往在綜合資產負債表一向呈現負資產及負儲備狀態,反而其運用公司賬內逾287.62億元派息。未來若需要進一步實物分派,亦將運用到前述儲備。這解釋了,今次分拆交易若成功,並且壯大公司及綜合儲備的話,將為日後對電盈股東更多派送,提供空間。長遠電盈的資產負債表谷大同時,若能夠作理想派送,自然有助減低股東對該公司及其管理層的怨氣,滅少遇到股東投反對票的阻力。

況且在電盈的通告中尚有微妙之處,既提到分拆後電盈從中取得資金用於增長中的企業方案及媒體業務,並且創造額外價值給股東,同時提到分拆所得款項有助電訊業務減債。若讀者細心留意,前述分派加上售股比例最多介乎35%至40%。但是若電盈擬保留55%股權,就會發覺有5%至10%之間的股權空間欠缺交待,實際上則有待電盈的解釋及演繹。這既可以理解成,電盈可以進一步減持電訊業務,然而若循發新股的方向理解,在邏輯上便可以解釋為何今次分拆可以幫助電訊業務減債。這在可能出現的加息周期中,尤為重要,可以減低利息開支蠶食盈利的狀況出現。

照過往經驗,若電盈由負資產轉為正資產,股價會有良好表現,並且會以倍計升。一般相信,純以較後時間公布的中期業績,便能扭轉當前負資產逾6億元的話,若配合可能分拆業務的消息及潛在的增值空間。電盈股價有望擺脫以前長期處於低谷的局面。