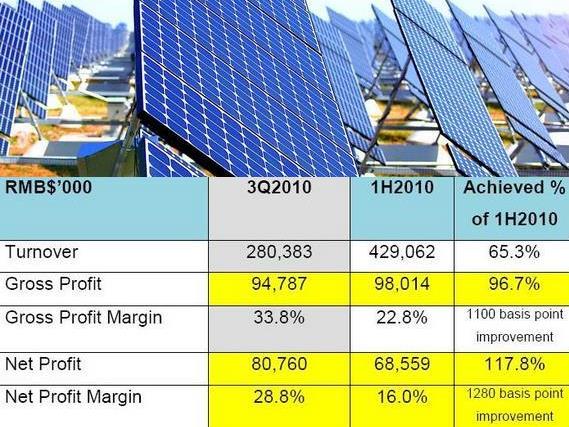

COMTEC SOLAR Systems Group Ltd (HK: 712) saw its third quarter net profit surge to 80.8 mln yuan on revenue of 280.4 mln.

The Shanghai-based solar wafer maker, which went public in Hong Kong in October 2009, had no year-earlier figures to provide, but did manage to outdo the first half bottom line in the July-September period on continued strong global demand, Comtec’s CFO told NextInsight.

Gross margins at the solar ingot firm put in a very bright performance, rising to 33.8% in the third quarter from 22.8% in the first six months.

Meanwhile, July-September net profit margins jumped even faster to 28.8% from 16.0%.

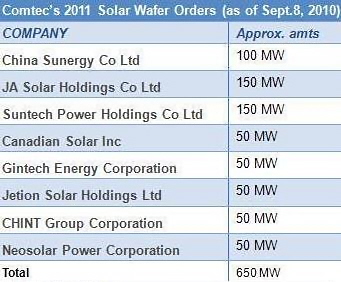

And the company saw no slowdown in orders, as currently Comtec had inked orders for 650 MW in wafer supply deals for 2011 out of an expected end-2011 total production capacity of 1,000 MW.

“We were somewhat pleasantly surprised by our third quarter results, but we also experienced strong demand and price increases in the first half. I think one of the best things to take away from these quarterly results is that we are still doing very well at maintaining our production costs,” CFO Keith Chau told NextInsight in an interview.

He also said that the monocrystalline solar wafer maker continues to maintain a healthy balance sheet with net cash position of 299.5 mln yuan, which included cash and cash equivalent of 468.8 mln and short-term bank loans of 169.3 mln in the third quarter.

The company launched its IPO in Hong Kong late last year to expand production capacity, fund raw material purchases and finance R&D, especially of its 125mm and 156mm wafer technologies.

Mr. Chau said that the company was committed to cost controls, even in a period of rapid capacity expansion and sales growth.

“Our improved margins are testimony to our tight control over operating expenses, which also allowed us to expand third quarter net profit that even outperformed that of the first six months. We also expect strong margins for the current quarter.”

When asked if sustained strong demand from solar cell/module makers, especially in Europe, would chase raw material costs higher, he said that Comtec’s strengthening margins proved that selling prices were keeping pace with silicon and other upstream inputs.

“We have seen that raw materials will change in line with wafer prices, and wafer prices are strong.”

A significant market for Comtec’s solar wafers and ingots is the EU, a region currently reducing subsidies to companies there as part of its FiT (Feed-in tariff) program.

However, Comtec was not overly concerned about the scheme.

“We believe it is reasonable to have FiT, and we are not really worried about the subsidy cuts. We fully expected the lower subsidies and were prepared, and we feel it is good for the long-term health of the industry in the EU,” Mr. Chau said.

However, Comtec realized that selling prices would not always remain at current levels but thanks to its effective cost controls, long-term contract fulfillments and flexible production, it was confident that it was prepared.

'10% reasonable net profit margin'

“Selling prices may become somewhat weaker going forward, but we feel that a reasonable gross profit margin in this scenario would be 20% and a reasonable net profit margin would be 10%, and business is sustainable at these marks. But as our latest results show, we are currently well above both of these levels,” he said.

The company’s results were released late Tuesday and at the time Mr. Chau said he had not yet seen corresponding sales and profit figures from his regional competitors.

“I haven’t looked at their most recent results but I expect that Comtec will be one of the best GPM performers among them.”

When asked how Comtec planned to spend its hard-earned profits from a very strong quarter, he said that the future growth of the newly-listed company was the most important consideration at this time.

“We have a reinvestment strategy, so no year-end dividend is planned. Also, investors should expect a roadshow to coincide with these results.”

In the company’s third quarter earnings statement, Comtec CEO and Chairman John Zhang said: "The outstanding 3Q2010 result highlighted that demand on quality wafers remain robust. Customers are still requesting us to offer them more allocation from our 2011 supply.

“We believe wafer demand remains healthy due to faster module and cell supplier recent capacity expansion. Our sales momentum is likely to remain strong in 2H2010 and we can look forward to another excellent performance in FY2010.”

The Chairman was also very bullish on the industry going forward.

"We also have confidence in the solar business in the coming years. The FiT Policy cuts in European countries will not harm the overall health of the solar industry but will rather help it mature. We will maintain our expansion plan for 1GW and beyond and continue striving to make Comtec Solar a world leader in the monocrystalline solar wafer industry."

According to a recent UBS report, most suppliers are expecting robust solar module demand through 2011 and indicated firm pricing through mid-2011 despite upcoming subsidies cuts in Germany and Italy.

UBS also estimates 2011 solar demand will be 19GW, up 17% year-on-year, saying this spells “promising prospects” for Comtec Solar ahead.

Comtec Solar is a Shanghai-based monocrystalline solar ingot and wafer manufacturer. Founded in 1999, it is one of the first manufacturers in China able to mass produce 156mm x 156mm monocrystalline solar wafers with a thickness of approximately 170 microns.

See also:

COMTEC SOLAR: What Analysts Now Say...

COMTEC: Thin Wafers, Thick Margins