Excerpts from latest analyst reports…..

CIMB maintains BROADWAY INDUSTRIAL’S target price at $1.86

Analyst: Jonathan Koh

We have left our FY10-12 profit forecasts intact and maintain our target price of S$1.86, set at 8x CY11 P/E (within its 5-year trading band). We expect stock catalysts from: 1) further expansion of its non-HDD component sales; and 2) upside surprises in dividends.

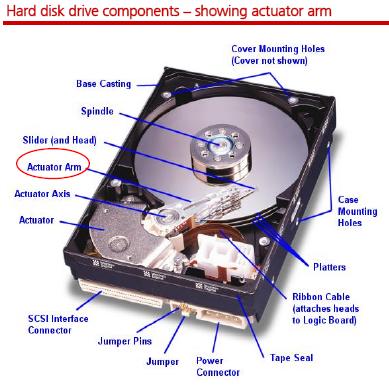

• HDD component business tracking below seasonal strength. We understand from Broadway and other HDD component suppliers that the HDD industry is likely to book sub-seasonal growth this year due to inventory adjustments and a slowdown in consumer notebook PC shipments. Qoq, however, there should still be marginal growth.

• Non-HDD component business to the rescue. Positively, Broadway’s non-HDD component business continues to do well as a result of continuous strength in the semiconductor equipment industry.

The completion of its acquisition of Atlantec’s Suzhou facilities will help to increase its non-HDD component capacity in 4Q10. Its foam packaging business is also benefiting from seasonal strength in 2H10.

Recent story: ARMSTRONG, BROADWAY: Takeover action & ...implication

RBS has a 'sell' on TIGER AIRWAYS on pilot exodus, flights cancelled; target price $1.58 (down from $1.95)

Royal Bank of Scotland Asia Securities (Singapore) analyst: John Rachmat

Tiger Airways has been cancelling a high percentage of its flights recently. We suspect this is caused by a shortage of pilots region-wide, a problem likely to persist in the medium term. We are therefore cutting our 2011-13 earnings forecasts by 19-34%, and we downgrade our recommendation to Sell.

In our note, Surprise capacity reduction, published last week, we highlighted a media report that over 20 pilots have left Tiger Airways since June over pay issues.

A strong recovery in the aviation sector had sparked a hunt for pilots, air crew and engineers, and the news article went on to say that Tiger’s departing pilots typically receive 30% higher compensation in their new jobs.

Tiger management confirmed this news, but also stated that it is recruiting replacement pilots from Mandala Airlines (an Indonesian budget carrier) and others, such that the company does not face any shortage of pilots for its day-to-day operations.

High cancellation rate of flights out of Changi Airport

However, we have been closely monitoring Tiger’s flight cancellations out of its home base in Changi Airport since that news broke, and we found that its cancellation rate of 14.8% is significantly higher than that of Valuair/Jetstar (7%) and AirAsia (1.8%) departing out of the same airport. We studied management’s explanation (technical problems with one aircraft plus out of date flight information) and found it unable to account for the breadth and frequency of the flight cancellations. We therefore suspect that the pilot shortage remains an issue, with negative implications for Tiger’s earnings outlook.

Surprise capacity reduction

We also see the unexpected news that Tiger will be leasing out two A319 aircraft (currently operated out of Singapore) to the Philippines-based Southeast Asia Airlines (SEAIR) as another indication of Tiger’s difficulty in staffing its current fleet operating out of Singapore.

Negative earnings implications

Two implications: (a) we cut our expectation of fleet expansion from 20 to 12 aircraft over the next three years, and (b) we raise our unit wage cost increase this year to 8% (from 3.7%). As a result, we cut our 2011-13 earnings by 19 to 34%, lower our target price by 19% to S$1.58 and downgrade our recommendation to Sell.