Religare analyst: Yan Ke (left)

Religare analyst: Yan Ke (left)Singapore-listed Giken Sakata (Bloomberg Ticker: GSS SP) has transformed into an onshore oil field play post its acquisition of Indonesian oil & gas assets via share acquisitions in Cepu Sakti Energy (CSE).

While GSS’s legacy business is precision machining and engineering, the listed company has now become primarily an Indonesia onshore oil field company due to its announced acquisitions.

Sydney Yeung, recently-appointed CEO of Giken Sakata. NextInsight file photo.The company’s initially acquired oil fields, named Dandangilo-Wonocolo and Tungkul, are located in Central Java and already producing oil.

Sydney Yeung, recently-appointed CEO of Giken Sakata. NextInsight file photo.The company’s initially acquired oil fields, named Dandangilo-Wonocolo and Tungkul, are located in Central Java and already producing oil. CSE (via PT Ceput Sakti Energy, PT CSE) holds exclusive rights to cooperate in conducting operations for extracting oil from both fields and in return has the rights to 80% of revenue arising from oil produced, with the remaining 20% shared with local cooperatives (KUD/BUMD).

PT CSE, under GSS, later acquired additional fields, named Kawengan, Trembul, and Gabus.

Post-acquisition of CSE, GSS effectively owns 51% of CSE, and hence has a 41% economic interest in the oil produced from the oil fields via its CSE stake. A qualified professional report by the firm Senergy (a member of the Loyd’s Register Group) indicates that the fields have 1P and 2P gross reserves of 5.6 million barrels and 9.6 million barrels respectively.

Including the three most recently acquired fields, for which a Senergy report has yet to be released, we estimate additional 2P reserves based on our model assumptions. This implies estimated gross total 2P reserves of 23.8mmbls.

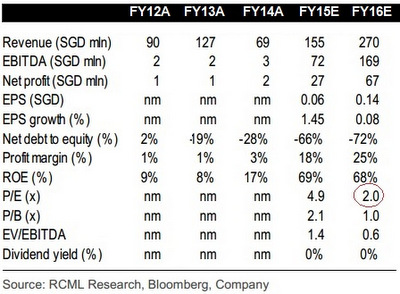

|

|