Excerpts from analysts' reports

Maybank Kim Eng says 'overweigh' China's water sector, buy HanKore and SIIC

Analyst: Wei Bin

Analysts checking out water-treatment facility of HanKore. File photo.Great interest in HanKore and SIIC

Analysts checking out water-treatment facility of HanKore. File photo.Great interest in HanKore and SIIC

We met over 20 clients during our recent marketing trips in Singapore and Hong Kong.

Broadly, investors agreed with our investment thesis amid buoyant interest in China’s water sector.

Maybank Kim Eng says 'overweigh' China's water sector, buy HanKore and SIIC

Analyst: Wei Bin

Analysts checking out water-treatment facility of HanKore. File photo.Great interest in HanKore and SIIC We met over 20 clients during our recent marketing trips in Singapore and Hong Kong.

Broadly, investors agreed with our investment thesis amid buoyant interest in China’s water sector.

There was greater interest in the municipal water players versus industrial water players, based on our deeper discussions on Hankore Environment and SIIC Environment.

Discussions focused on room for further expansion in sector ROE and how sustainable would industry consolidation be.

With stocks trading in excess of 20x one-year forward P/E, it was hardly surprising to note that the main pushback from investors was their high stock valuations.

Discussions focused on room for further expansion in sector ROE and how sustainable would industry consolidation be.

With stocks trading in excess of 20x one-year forward P/E, it was hardly surprising to note that the main pushback from investors was their high stock valuations.

Arguably, current high valuation can be justified by robust EPS growth and potential for more EPS-accretive M&As.

In our view, the sector is poised for a golden era in the next three years, with rising water tariff, strong government policy support and industry consolidation fuelling rapid growth.

We believe sector ROE is on a structural uptrend supported by a 15% sector EPS CAGR over FY14E-16E.

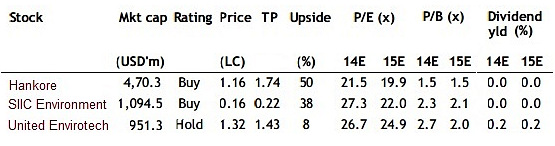

We continue to prefer companies with high-quality assets that generate recurring income stream such as Hankore Environment (TP adjusted to SGD1.74 due to recent 10-for-1 share consolidation) and SIIC Environment.

Maintain our BUY rating on HanKore (TP adjusted to SGD1.74 due to recent 10-for-1 share consolidation) and SIIC (TP unchanged at SGD0.22).

We have a HOLD rating on UENV (TP unchanged at SGD1.43).

We believe sector ROE is on a structural uptrend supported by a 15% sector EPS CAGR over FY14E-16E.

We continue to prefer companies with high-quality assets that generate recurring income stream such as Hankore Environment (TP adjusted to SGD1.74 due to recent 10-for-1 share consolidation) and SIIC Environment.

Maintain our BUY rating on HanKore (TP adjusted to SGD1.74 due to recent 10-for-1 share consolidation) and SIIC (TP unchanged at SGD0.22).

We have a HOLD rating on UENV (TP unchanged at SGD1.43).