Excerpts from analysts' reports

|

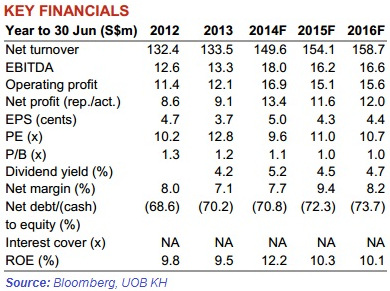

UOB Kay Hian initiates coverage of cash-rich Lantrovision Analyst: Loke Chunying  We initiate coverage on Lantrovision with a BUY recommendation and target price of S$0.645. Lantrovision is principally engaged in the installation and maintenance of structured cabling systems for the finance and IT sectors. We initiate coverage on Lantrovision with a BUY recommendation and target price of S$0.645. Lantrovision is principally engaged in the installation and maintenance of structured cabling systems for the finance and IT sectors. With over 20 years of operational history, Lantrovision has formed and maintained strategic relationships with a group of blue chip clients that include major banks and global MNCs. With a net cash position of S$82.1m that forms 64% of current market cap, Lantrovision is trading at a compelling valuation of 4.0x (ex-cash) FY15F PE, which is at a steep 52% discount to its peers’ average trailing 12M PE of 8.3x. |

CIMB lifts earnings forecast and target price of Nam Cheong (to 44 cents)

Analyst: Yeo Zhi Bin (left) Analyst: Yeo Zhi Bin (left)

|

|||

2015 delivery programme unveiled Nam Cheong has unveiled details for its 2015 delivery programme – it aims to deliver 35 vessels in that year (vs. 30 in 2014). We note the slant towards 6,000 bhp AHTS (~40% of the programme and a successor to the 5,000 bhp AHTS), which is touted by industry watchers to be the workhorse of the near future. In our view, this reflects Nam Cheong’s ability to keep its ears close to the ground and read vessel trends accurately.  Nam Cheong CEO Leong Seng Keat: "Having achieved record order wins in 2013, we expect the sales momentum to continue this year as we tap into a resurgent market.” File photo.Not as risky as it seems Nam Cheong CEO Leong Seng Keat: "Having achieved record order wins in 2013, we expect the sales momentum to continue this year as we tap into a resurgent market.” File photo.Not as risky as it seems Management is cognisant of the higher risks associated with its build-to-stock business model that earns more lucrative gross margins of 15-20% than the ~10% for the build-to-order business. Thus, management has always been cautious and maintained a worst-case scenario operating philosophy. In this aspect, Nam Cheong focuses on shallow water production assets which will be more resilient than deepwater exploration assets, which are at the highest risk of capex cut. The group stays in a healthy financial position (1Q14 net gearing of 0.35x) to ensure that it is able to absorb its newbuilds, in the event of a severe downturn. Lastly, it operates an asset-light model by subcontracting 80% of its orders to Chinese yards. Recent story: NAM CHEONG -- buy, target 48 c, BOUSTEAD --- hold, $2.00 target

|

|||