Excerpts from analysts' reports

UOB Kay Hian highlights potential of REX INTERNATIONAL

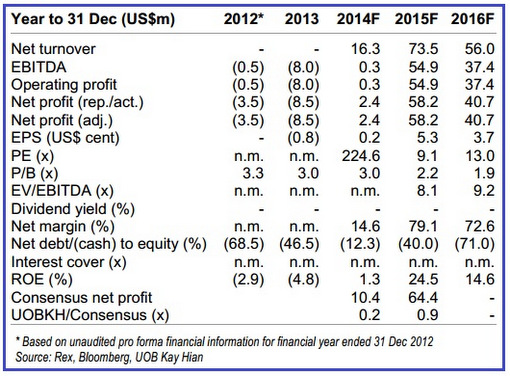

Analyst: Loke Chunying

Mans Lidgren, CEO of Rex International.

Mans Lidgren, CEO of Rex International. NextInsight file photoWith its access to the proprietary Rex Technologies (RT), Rex International (Rex) offers investors the exciting rewards of oil exploration at lower risks and costs, with exploration success rate claims of more than 50% as compared with the industry’s 10-15%.

With the recent oil find in East Oman (where oil has never been discovered before), RT shows great promise, helping Rex to secure strategic partnerships and concessions along the way.

• Target price of S$1.27 is derived from the risked NAV of Rex’s oil concessions, using the expected monetary value methodology based on average rates of exploration success from conventional methods of analysis.

We have not imputed improved success rates with the use of RT, which may provide further upside to our target valuation if RT proves to be successful.

Recent story: REX International: Stock's up on oil hit in second Oman drilling

Lim & Tan Securities points to major transformation of GuocoLeisure

GuocoLeisure, which has long been operating hotels in London (above), now seeks to become a global hotel operator with presence in 100 major cities by 2023. Photo: CompanyWe are initiating coverage on Guocoleisure (GLL) with a BUY rating as

GuocoLeisure, which has long been operating hotels in London (above), now seeks to become a global hotel operator with presence in 100 major cities by 2023. Photo: CompanyWe are initiating coverage on Guocoleisure (GLL) with a BUY rating as a. management has turned bullish and expects to experience an acceleration of pricing power across their London Hotels on the back of record occupancy and room rates;

b. the transformation into a global hotel operator with presence in 100 major cities by 2023 is helmed by a new CEO who has a strong track record of delivering results and he and his team has been awarded 73.5mln GLL options with an exercise price of 86 cents each to incentivise them to succeed);

c. the transformation will grow GLL’s presence from 2 cities to 100 cities and drive revenue and profit growth significantly;

d. the transformation process in the next few years would put them in the same league as global hotel operators such as Hilton, Starwoods and Marriot, potentially bringing about a re-rating of its valuation closer to industry average of 15x EV/EBITDA;

e. the transformation process allows GLL the option to go asset-light from owned hotels to managed hotels, boosting its ROE, ROA and earnings trajectory, as well as giving GLL the option to recycle assets;

f. GLL is currently trading at a large 50% discount to our sum of the part estimates of $1.70 and an even more massive 73% discount if the company successfully transforms into a global hotel operator over the next few years;

g. Quek Leng Chan’s (QLC) S$1.25 per share failed privatization offer in 2005 and his 86.5mln (6.53% of the company) open market purchases from 2008 till 2013 (bringing his stake to 66.7%) provides strong clues to the deep value of the company.

Previous story: GUOCOLEISURE: 3Q loss but UOBKH and Lim & Tan upbeat on stock