JP Morgan: Several concerns weighing down developers

JP Morgan said it recently met with investors marketing on the Hong Kong real estate sector to highlight opportunities among Hong Kong’s listed developers.

“Views on the sector are quite mixed, with some long-only investors willing to buy developers, while others are worried about interest rate hikes, policy risks and potential residential price drops,” JP Morgan said.

The research house said there are mixed views on Hong Kong developers.

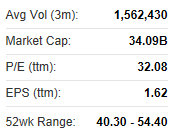

JP Morgan likes SGX-listed Hongkong Land.

JP Morgan likes SGX-listed Hongkong Land.

Photo: Company“While most investors agree that valuations of HK developers are attractive, there are mixed views on whether to buy the developers now.

“Those who are more positive on the sector are mainly the property specialists who are thinking to switch out from Japan to Hong Kong and China given the valuation gap.

"The most bullish investor suggested farmland conversion could be a potential driver for NAV upgrade.”

JP Morgan added that it thinks investors are satisfied with their holdings in the Hong Kong Real Estate Investment Trusts (REITs) sector.

It emphasized that key investor concerns of late include: 1) impact of policy measures on the market and the company; 2) pressure on residential development margin; 3) strategy on investment properties, and 4) China strategy.

“With the HK government ongoing offering of residential sites, the company views there are more opportunities in HK than in China.

HK Land recently 7.26 sgd“While new investment properties will continue to add to the rental portfolio when they get completed, it is possible to divest some noncore investment properties if valuations are attractive.”

HK Land recently 7.26 sgd“While new investment properties will continue to add to the rental portfolio when they get completed, it is possible to divest some noncore investment properties if valuations are attractive.”

JP Morgan said it thinks most major developers (including SHKP, Henderson Land, New World Development and Sino Land) are still trading at attractive valuations of 38-45% discounts to Dec-13 NAV.

“Among landlords, we still like Singapore-listed Hongkong Land (SGX: HKLD; ‘Overweight’) on expectations of a Central office recovery, followed by Hysan (HK: 14; ‘Overweight’).”

UBS: China property prices need to stabilize to avoid more tightening

UBS Investment Research has summarized key takeaways from its discussions with around 30 property companies and experts on Hong Kong and China’s real estate sector. Some analysts like property managers like Prosperity REIT whose before-and-after Hong Kong rooftop real estate improvement project is shown above. Photos: Prosperity REIT

Some analysts like property managers like Prosperity REIT whose before-and-after Hong Kong rooftop real estate improvement project is shown above. Photos: Prosperity REIT

“For China property, prices need to stabilize to escape more tightening,” UBS said.

Following strong Q1 2013 sales, developers expect sales to slow in April due to the lack of new launches and pull-forward of demand in March, before implementation of new rules, the research house said.

Margins are expected to stay flat from 2012 levels and are unlikely to rebound.

Preferred picks are Guangzhou R&F, Shimao, Country Garden, COLI, CKH, NWD and SHKP.

The implementation of various stamp duties has weakened market sentiment and reversed rising home prices.

“Midland & the developers expect primary sales to fall further in May/June after enactment of the new 1st Hand Sales Ordinance. In line with our projection, Midland forecast HK prices to fall 5-10% over the rest of 2013,” UBS said.

Credit Suisse is maintaining its 'Market Weight' call on Hong Kong’s property sector. NextInsight file photoCredit Suisse: HK property sector kept ‘Market Weight

Credit Suisse is maintaining its 'Market Weight' call on Hong Kong’s property sector. NextInsight file photoCredit Suisse: HK property sector kept ‘Market Weight

Credit Suisse said it is maintaining its “Market Weight” call on Hong Kong’s property sector.

“We have noted good market response to the inventory clearance by developers in the last two months, with at least 6.3 billion hkd in proceeds from the sale of at least 580 units.

“We estimate that there are fewer than 1,000 launched-but-not-sold units in the market (excluding those by Hang Lung Prop),” Credit Suisse said.

The research house said it expects the discount being offered during the inventory clearance to be a one-off, and it is not indicative of upcoming launches.

“We do not see any major price-cut intention by developers yet.”

Compared with two months ago when the market was weighed by the mortgage rate increase by larger banks, rates show signs of stabilization.

“Fixed rate mortgage products appear not to be popular among the borrowers, which reflects that they are probably not expecting interest rates to go up again, in our view,” Credit Suisse added.

“Given the good market response to the inventory clearance, we expect developers to be more confident in launching new projects. We reiterate our preference for developers at this level.”

Deutsche Bank: China property demand in Tier 2&3 markets strong

Deutsche Bank said its analysts recently spent two days in Zhengzhou, the provincial capital of Henan Province, to monitor property trends in China’s Tier 2 and 3 cities.

“Overall, the trip reaffirmed our view that the property markets in most Tier-2/3 cities in China are driven primarily by solid end-user demand, stemming from continued GDP growth and urbanization.

Greentown is a top 'Buy' with Deutsche. Photo: Greentown“With ASPs rising at a moderate pace, we also do not see significant tightening by local government on top of the central government's measures, and we expect continued solid sales momentum ahead for the professional developers, like China Central Real Estate,” Deutsche said.

Greentown is a top 'Buy' with Deutsche. Photo: Greentown“With ASPs rising at a moderate pace, we also do not see significant tightening by local government on top of the central government's measures, and we expect continued solid sales momentum ahead for the professional developers, like China Central Real Estate,” Deutsche said.

The German research house said it saw a solid residential property market supported by strong end-user demand.

In 2012, residential sales in Zhengzhou amounted to 69 billion yuan, up 13% y-o-y.

Among the 40 major cities in China, Zhengzhou ranked 17th in residential sales value and 11th in volume, highlighting its significance.

“According to local management/salespeople, residential sales in Zhengzhou have remained solid YTD, and sell-through rates are high for city-centers projects.

“According to local management and salespeople, with HPRs in place, the majority of the homebuyers in Zhengzhou are end-users, from both within Zhengzhou and other parts of Henan Province, and the strong end-user demand comes from continued strong GDP growth and rising urbanization in Henan, and the continued build-up of infrastructure by the central and local governments.”

Deutsche added that for the rest of 2013, more new launches are expected to come starting May, so sales volume in the primary market should be stronger during the rest of 2013.

Its top “Buys” are COLI (HK: 688), China Overseas Grand Ocean (HK: 81), China Resources Land (HK: 1109), Guangzhou R&F (HK: 2777) Greentown, China Central Real Estate (HK: 832), Kaisa and CC Land.

“The sector is now trading at NAV discounts, P/Es and P/Bs that are well below the historical average or close to ‘-1SD’ level of the historical (2006 to date) range – attractive, in our view.

“We expect a stable property policy environment for the rest of 2013, with more fiscal spending and micro-level stimulations by the government to boost the economy.”

Goldman Sachs: TSINGTAO kept ‘Neutral’

Goldman Sachs said it is maintaining its “Neutral” recommendation on Tsingtao Brewery (HK: 168) with a target price of 49.2 hkd (recent share price 52.85) after “in-line” results. Photo: Tsingtao BreweryTsingtao reported first quarter net profit of 488 million yuan, up 8.3% y-o-y, driven by strong 12.7% sales growth and 0.2 percentage point EBIT margin expansion to 9.6%.

Photo: Tsingtao BreweryTsingtao reported first quarter net profit of 488 million yuan, up 8.3% y-o-y, driven by strong 12.7% sales growth and 0.2 percentage point EBIT margin expansion to 9.6%.

“While largely inline, we consider this to be a solid set of results given our expectations of broad-based weakness in the quarter,” Goldman Sachs said.

Revenue grew by 12.7% y-o-y, driven by 11.7% volume growth (slightly ahead of management’s guidance of 11%) and 1.1% ASP (below our full year expectation of 3%).

“We think Tsingtao continued to gain market share, outperforming Yanjing's 7% y-o-y volume growth (peers Anheuser-Busch InBev and China Resources Snow are due to report results on April 30 and mid-May, respectively).”

Goldman Sachs said it is maintaining its “Buy” rating on Tsingtao Brewery’s A shares.

Morgan Stanley: TSINGTAO’S 28x 2013e P/E ‘unattractive’

Tsingtao reported 1Q13 results with 12.7% y-o-y growth in sales and 8.3% growth in net profit.

“Top-line growth was slower than our full-year estimates of 16% sales growth and 14% net profit growth. Key trends would be set during peak season in 2Q/3Q, especially for pricing and promotional strategies.

“At 28x 2013e P/E, we find the stock unattractive,” Morgan Stanley said.

Tsingtao recently 52.1 hkdTop-line growth was mainly driven by volume growth of nearly 12%.

Tsingtao recently 52.1 hkdTop-line growth was mainly driven by volume growth of nearly 12%.

“Product mix should have continued to skew slightly to non ‘Tsingtao’ brand (‘Tsingtao’ brand volume increased 10% y-o-y vs 4.0% for other brands).”

Gross margin expanded 2 percentage points to 33.2% thanks to ASP increase by 1.1 ppt and some cost savings.

“However, the gain in gross margin was largely offset by higher opex ratio (up 1.8ppts) with higher distribution and selling costs.”

Morgan Stanley reiterates its view that stiff competition among top brewers for market share should slow earnings growth in 2013/14, before the industry reaches the phase of meaningful improvement in profitability driven by higher level of consolidation.

“We think Tsingtao’s 2Q13 opex ratio should remain high so it can stick to its volume growth target (CAGR 12.5% in 2012-14, to reach 10 mln kiloliters sales volume by 2014).

“In particular, we note that CRE continues its price discounting strategy in 1H13.”