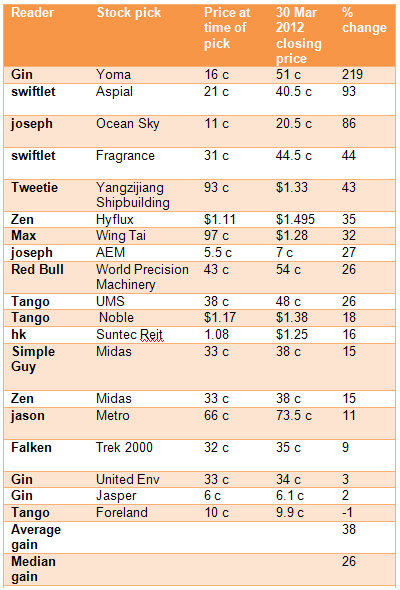

CONGRATS TO a bunch of NextInsight readers! The end of 1Q of 2012 has brought about juicy gains for their stock picks, with one small exception (see table on the right).

In late 2011 and early 2012, a dozen readers had highlighted their favourite stocks in an article Hey brother, what are your best stock ideas?

Their stock picks have gained 38% on average, outpacing the 14% gain in the Straits Times Index year to date.

Here are the top three investors:

> ‘Gin’ picked Yoma Strategic, which has soared 219% since he mentioned it in the article.

Gin must have a strong does of foresight in expecting Yoma shares to turn hot because of its Myanmar connection.

He gave as reason for his pick: “Myammar opening up its market, potential gain in property and influx of tourist will make the stock attractive since it is also in the hotel business.”

But his two other picks – Jasper and United Envirotech – didn’t turn out so shiny with 2-3% gains only.

No one, including Gin, can hit bull’s eye all the time, it would seem.

> ‘swiftlet’ hit the bull's eye twice, though.

His/her picks (Aspial and Fragrance) soared wildly with 93% and 44% gains, respectively.

Again, as in Yoma's case, Fragrance made strong gains because it had a catalyst – in the latter case, the spin-off of its hotel arm known as Global Premium Hotels for a separate listing on the stock exchange.

Ditto for jeweller-cum-property developer Aspial Corp, which is considering a spinoff of its financial services business (read: Maxi-Cash) through a listing on Catalist.

Another catalyst for Aspial stock was the sterling $45.3 million net profit announced in February for FY2011 for the group, up from $4.8 million the year before.

> 'joseph' scored with Ocean Sky, a specialty apparel manufacturer with supply chain management (SCM) capabilities, which rocketed up 86%.

'joseph' relied on hard financial facts for his pick:

1) Current PE 4.3 forward pe 3.1.

2) NTA 22.16.

3) Dividend yield 14.5%.

4) Singapore-ased company.

5) Cash backing per share 8cts.

6) 52 week high 22cts, low 10cts, therefore low risk.

Would all three of you like to tell us your stock picks for 2Q?

How about the rest of you readers out there? Come on, share your best stock ideas below in the Your Comments section.

Remember to give reasons and state also the stock price at the time of your writing for easy reference. Happy investing!

1) MDR (Previously ACCS) - 9 continuous quarters of profits, no debt and paying dividends though is insignificant. Looks like is a turnaround story. Share price fell from a high of 8 cents to 1.5 cents now. Possiblity of going back to 8 cents? Given that company has been making progress in revenue generating and debt free now.

2) Sin Heng - ride on the myammar story. Company has been profitable, rental and salling construction equipment. IPO price 26 cents. Recently, announced a joint venture to explore business opportunities in myammar.

There is a catalyst -- Lian Beng (43 cents) will be listing 2 subsidiaries likely in this quarter. Good for unlocking value...Like Aspial & Fragrance.... this Ah Beng could, imho, yield not just for cap gain but a special dividend. Ah Beng is very cash rich.

The listing is expected by analysts to raise $29 m. Now, already has cash of $185 m, some of which will be reserved for its property dev projects

Lian Beng has about $100 m in borrowings -- so net cash is about 16 cents. Stock’s attractive also cos of ex-net cash PER of ~ 2x FY12 ending June, and a dividend yield of ~ 3.7%, assuming Ah Beng doesn't give special div and maintains FY11 dividend of 1.6 cents.

Note that year to date, Lian Beng has risen from 35 cents to 43 cents, so 23% gain is already in the bag for those who bought 3 months ago in anticipation of a catalyst from the said IPO.

Please note that my comments are in relation to this specific article and therefore I am not lambasting other investing methods. But I must insist that any method used, whether they be TA-related, a hybrid or some other form of market timing, has to be consistent and is fully customized to that partcular practitioner. In other words, consistency over time is, to me, more important that having a nice large gain over a very short period of just 3-6 months.

Indeed you are right to say that FA is very hard work; then again if we do not put in time and effort how can we reasonably expect to achieve good returns? A simple analogy would be your day job where you have to literally slog and work hard to earn your salary - there is (literally) no free lunch! TA may seem "simpler" and "works" because we are currently in a bullish phase and stock markets have been rallying since the start of the year, which generally makes people feel as if making money is easy and not much effort is required. This is also the time when investors should feel the most cautious, as many companies cannot be purchased with a margin of safety and many speculative companies without good earnings and cash flows start to see massive % price rises.

You mentioned deep value plays and turnaround stories - and I would conclude that these are also an aspect of value investing; for you are simply trying to compute an intrinsic value to a business and purchase at a discount to that value, and then wait for Mr. Market to realize the gap. Investing is all about purchasing companies on the cheap based on what the businesses can generate in terms of cash flows and future earnings.

I don't know enough about Sing Holdings to make a comment on it, but I have held some companies for about 2-3 years before I've even seen a decent rise in share price, even as the business continues to do well. I have no qualms about doing so, as I also enjoy a very healthy yield in the meantime, and I can sleep well at night knowing the business is chugging along fine.

Your last statement shows precisely the kind of malady (sorry if I have to use this word) which permeates the stock market during bullish phases. Why should one obssess over stock prices for a mere 3 month-period? I have examined the businesses I own and companies such as Kingsmen, SIA Engineering and Boustead are moving along well in their business development efforts; thus I am confident that the business is doing fine and will continue to grow and generate cash flows. It is of no consequence to me if the share price stays depressed - in fact I would wish for it to go down more so that I can add to my holdings. Incidentally, much literature on investing has shown that a value portfolio generally underpeforms a bull market, sometimes very significantly. This is because I care more for protecting my downside than chasing for my upside.

Regards.

It’s such a pluralistic community, and different investors make their own choices with varying results. Yes, even the fundamental “I’m buying a business, not a stock” approach is not always a successful one. My friends who have Sing Holdings for the last two years wonder what afflicts this stock to cause it to lie in coma for the last two years even though its profit has surged. And I see a few stocks in your portfolio that are mentioned in your blog have not participated strongly in the recent rally since Dec2011.

Investing is about consistency and adopting a disciplined approach and prudent methodology in order to ensure that one protects their downside (margin of safety), rather than always focusing on one's upside. A time frame of at least 3-5 years should be adopted and an investor's returns should be computed using an annualized return basis (yield + capital gains) to see if it was indeed a good investment. More importantly, it is important to judge the investor based on a portfolio basis (i.e. how the portfolio performed) and not just based on the high % gains of one pick out of so many.

Finally, I don't think investors should feel happy when share prices rise. In fact, if you were a net buyer of equities and have youth on your side, you should (emphasis added) much prefer LOWER prices as a way to profitably increase your holdings in quality, well-run businesses over time.