Excerpts from latest analyst reports...

CICC says ‘high earnings visibility ahead’ for SOHO CHINA (HK: 410) ‘hold’; TP: 6.62 hkd

Analysts: Peter Bai, Anson Ning

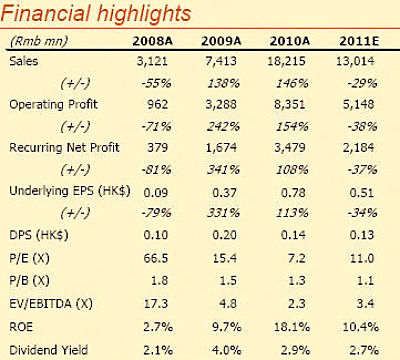

FY10 recurring EPS at RMB0.67/shr

SOHO China announced its FY10 revenue surged by 146% yoy to RMB18.2 bln, mainly du to the increase of both booked GFA (409k sqm, up 131% yoy) and ASP (RMB 44,524/sqm, up 9% yoy). Recurring net profit reached RMB 3,479 mln, ~18% above our estimate and representing a 108% yoy increase. Final dividend was RMB 0.14/shr.

Positives:

Good contracted sales at RMB 23.8 bln by end-Dec, up 74% yoy, with ASP at RMB 59,824/sqm. The projects Galaxy SOHO, The Exchange-SOHO and SOHO Nexus Center were the major contributors, with contracted sales at RMB 14.64 bln, 3.82 bln and 3.55 bln, respectively.

Healthy balance sheet: SOHO managed to maintain net cash position with net gearing ratio at -45.5% thanks to good presales in FY10.

Negative: Lower than expected net margin, which shrank 3.5 ppt to 19.1%.

Trends to watch:

Going forward, we believe the >RMB 18 bln carried-over presales (~RMB 6.7 bln already in presales deposits) will provide high earnings visibility for 2011 and 2012, and gross margin should be flat as the increasing land cost offset by the higher ASP.

Earnings revised up, HOLD maintained

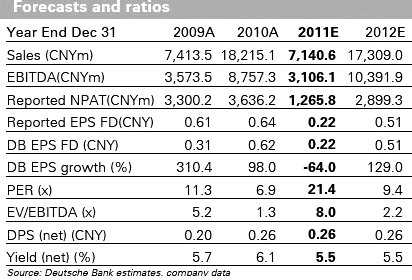

We revise 2011 recurring EPS to RMB 0.51/shr and introduce 2012 recurring EPS at 0.82/shr. We believe SOHO will likely see good presales in 2011, especially when the transaction in residential market is capped by house purchase restriction policy

See also: HANG LUNG PROPERTIES, SOHO CHINA: What Analysts Now Say...

Deutsche Bank reiterates ‘buy’ for SOHO CHINA (HK: 410) TP: 7.31 hkd

Analysts: Venant Chiang, Jason Ching, Tony Tsang

Tough market, good time for SOHO to expand

SOHO China's unique business model should allow the company to enjoy strong growth due to the growing commercial market in China. Management's proven execution capability and strong financial strength should provide the company with a great opportunity for future NAV growth despite a tough market, in our view. Reiterate Buy.

Core net profit up significantly by 108% yoy

FY10 results came in stronger than our expectations due to stronger sales booked during the period. Core earnings, excluding the revaluation gain on investment properties, soared 108% yoy to RMB3.5bn. Turnover jumped 146% owing to the substantial increase in area booked (up 131% yoy) and higher booked ASP (up 9%). Gross margin and net margin remained at a high level of 51% and 19%, respectively. SOHO China had a rich net-cash position of about RMB11bn at end-2010 and declared a full DPS of RMB0.26, implying a 5.5% dividend yield.

Strong cash + proven acquisition track record = NAV upside

SOHO China announced an aggressive expansion plan for 2011, spending RMB15bn (1.4x more than 2010) on project acquisitions in Beijing and Shanghai. We believe that the difficult operating context is a positive to SOHO China due to less competition, which should lead to a cheaper cost of acquisition. We see this as the key driver of its stock performance, as potential acquisitions could enhance NAV significantly when the China commercial space begins to receive its re-rating.

Attractively valued at a 42% discount to NAV with a high dividend yield

Our target price of HKD7.31 represents a 25% discount to our NAV of HKD9.75 (up from HKD9.40 due to the inclusion of new acquisitions). Our estimated NAV conservatively factors in flat commercial property prices from the 3Q10 level and no rental growth. The stock is well-supported by a dividend yield of 5.5%, which is one of the highest in the sector. Risks: execution in earnings delivery and stronger than expected tightening policy.

See also: CHINA/HK SHARES: A Shares Add A Percent, HK Two On Hot Properties