Combine Will factory in Dongguan. Photo by Leong Chan TeikCOMBINE WILL, listed on the SGX and working towards a dual listing in South Korea, is a one-stop ODM/OEM manufacturer for plastic, die cast and electronic assembly.

Combine Will factory in Dongguan. Photo by Leong Chan TeikCOMBINE WILL, listed on the SGX and working towards a dual listing in South Korea, is a one-stop ODM/OEM manufacturer for plastic, die cast and electronic assembly.

Among its shareholders is well-known Singapore investor 2G Capital.

Combine Will's products include premiums (an example would be small gifts that a global fast food chain store gives out along with customers’ meals), and digital consumer products.

It has five manufacturing plants in Dongguan and Heyuan, Guangdong Province, employing over 10,000 production workers and experienced managers – many of whom have been with the company for over 15 years.

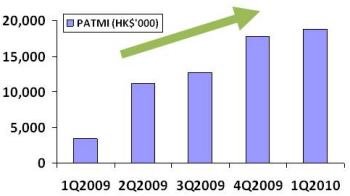

The company recorded profit after tax and minority interests of S$3.37 million for 1QFY10, which is 5.5 times higher than 1QFY09’s S$0.61 million.

To understand the profit drivers behind the strong growth, we visited the company’s manufacturing plants recently.

New Profit Growth Driver Net profit has been rising.According to Mr Simon Chiu, an Executive Director of Combine Will, the company’s key revenue and profit growth driver is a new high volume innovative household product – the automatic liquid-soap dispenser.

Net profit has been rising.According to Mr Simon Chiu, an Executive Director of Combine Will, the company’s key revenue and profit growth driver is a new high volume innovative household product – the automatic liquid-soap dispenser.

The company started to mass produce the dispensers in late 2009 for an international listed consumer goods giant with market capitalisation of over S$40 billion.

The product is considered to be “one of the high hopes for 2010 earning growth” of the customer, according to a news article on The Wall Street Journal, quoting the CEO of the customer.

The liquid-soap dispenser comes with an innovative touchless design which brings convenience and safety for users. The product dispenses liquid soap when its sensor detects hand motion under the nozzle.

This feature is ideal for users who do not wish to touch the soap pump. It also reduces the risk of virus transmission. This benefit is especially important during pandemic outbreaks such as SARS and avian flu.

Simon pointed out that the structural design of the dispenser is complicated.

The in-house team spent months with the client to evaluate and refine the dispenser design. The final product contains more than 50 individual parts, including electronic components.

Established Customer Base

Automating the spray painting process. Photo by Damien ChongOne of the critical success factors for Combine Will is its strong bond with customers. This was built upon its long working relationship with major customers, its consistent product quality and its ability to keep production costs low.

Automating the spray painting process. Photo by Damien ChongOne of the critical success factors for Combine Will is its strong bond with customers. This was built upon its long working relationship with major customers, its consistent product quality and its ability to keep production costs low.

Combine Will has been working closely with its major customers for many years. One of such customer is a marketing agency firm which supplies premiums to big companies such as global fast food chain stores.

Combine Will has been manufacturing premiums for that marketing agency going back as far as 1992. Such loyal customers have provided the relatively stability of volumes and revenue for Combine Will over the recent economic and financial crisis.

Thus, the company has always been profitable and could afford to pay $0.01 dividend since its listing in 2008.Consistent product quality is one of the top reasons why customers choose to work with Combine Will.  Simon pointed out that the company received seven awards, including “Overall Performance Award” in 2009 from one of its major customers for achieving high standards of product quality.Combine Will was able to keep its production costs low through product innovation and machine automation.

Simon pointed out that the company received seven awards, including “Overall Performance Award” in 2009 from one of its major customers for achieving high standards of product quality.Combine Will was able to keep its production costs low through product innovation and machine automation.

During the factory tour, Simon pointed out an example of a design enhancement by its R&D team, which resulted in the reduction of the number of screws required to manufacture a particular product model. This in turn translated into significant cost savings for the client.

Automation is another key advantage, particularly in the relatively labour intensive industry like Combine Will’s. According to Simon, Combine Will has the highest level of automation among its peers.

A good example is automating the hand-spray process for certain parts; each time, four parts can be painted by the automatic machine comparing with one part at a time with the traditional hand-spray painting. The company believes that there are only a few competitors in China that have adopted similar process presently.

Proposed Dual Listing in Korea

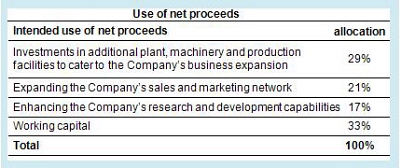

Combine Will is raising funds for business expansion and working capital purposes through Korean dual listing. The company plans to do a 10-to-1 share consolidation exercise and offers 11 million new ordinary shares on KOSDAQ, which represented 25.1% of the enlarged share capital.

The estimated amount of net proceeds would be S$21.46 million (see table) based on the minimum issue price of S$2.30 per share. Our calculations show that the minimum issue price offers a 24% premium to current share price after share consolidation.

Set for Solid Phase of Growth

Combine Will is on track to record strong revenue in the current financial year based on the new high volume innovative product. Together with the baseline earnings from the loyal customers, chances are that the company will be able to grow its business to a new level.